Table of Contents >> Show >> Hide

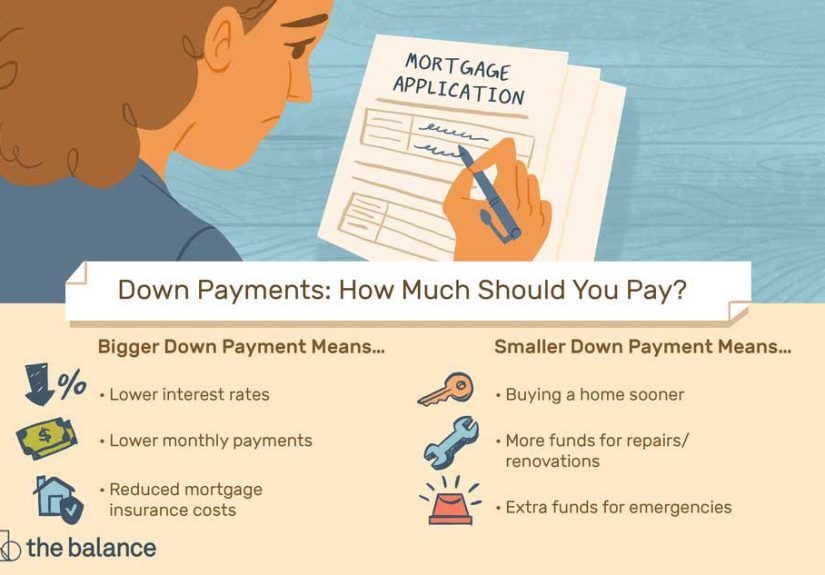

- What Is a Down Payment?

- How Down Payments Work in Real Life

- Do You Really Need 20% Down?

- Common Home Loan Down Payment Ranges

- How Much Should You Put Down?

- What Else You Need Besides the Down Payment

- When a Larger Down Payment Makes Sense

- When a Smaller Down Payment Might Be Smarter

- How to Choose the Right Number for You

- Down Payments on Cars Work the Same Basic Way

- Common Down Payment Mistakes to Avoid

- Real-World Experiences and Lessons From Buyers

- Final Thoughts

If the phrase down payment makes you picture a giant sack of cash, a dramatic sigh, and a lender nodding like a wizard granting access to a secret chamber, welcome. You are among friends. A down payment can feel like the most intimidating part of buying a home, mostly because it is the part that demands actual money instead of hopeful vibes.

But here is the good news: down payments are not one-size-fits-all, and the old idea that you absolutely must put 20% down is more myth than law. For some buyers, a bigger down payment is smart. For others, it is financially reckless to drain every dollar of savings just to avoid mortgage insurance. The “right” number depends on your loan type, your monthly budget, your emergency fund, your timeline, and your tolerance for financial drama.

In this guide, we will break down how down payments work, what they actually change, and how much you may want to put down. We will also walk through real-world examples, common mistakes, and the kind of practical advice people wish they had heard before they started touring open houses and emotionally adopting kitchen islands.

What Is a Down Payment?

A down payment is the upfront cash you contribute toward a purchase while borrowing the rest. In home buying, it is your initial stake in the property. If a house costs $400,000 and you put down 10%, your down payment is $40,000 and your mortgage covers the remaining $360,000.

That sounds simple, and mathematically it is. Financially, though, a down payment pulls several levers at once. It affects:

Your Loan Amount

The more you put down, the less you borrow. Less borrowing usually means a lower monthly principal-and-interest payment and less interest paid over the life of the loan. Your wallet tends to appreciate this arrangement.

Your Loan-to-Value Ratio

Lenders look closely at your loan-to-value ratio, often shortened to LTV. This is the percentage of the home’s value you are financing. Put down 20%, and your LTV is 80%. Put down 5%, and your LTV is 95%. Lower LTV usually means less risk for the lender, which can lead to better loan terms.

Your Mortgage Insurance Costs

If you put down less than 20% on a conventional mortgage, you will typically pay private mortgage insurance, or PMI. On FHA and USDA loans, other forms of mortgage insurance or guarantee fees generally apply. These costs do not build equity for you. They are there to protect the lender, not to reward your excellent taste in split-level colonials.

Your Cash to Close

This is where many buyers get surprised. Your down payment is not the only money you need upfront. You also need cash for closing costs, prepaid items, and sometimes reserves. So when you proudly announce, “I saved enough for 10% down,” the home-buying universe may gently reply, “Cute. Keep going.”

How Down Payments Work in Real Life

Let’s use a simple example. Say you want to buy a $350,000 home.

If you put down 3%, that is $10,500. If you put down 10%, that is $35,000. If you put down 20%, that is $70,000. The higher the down payment, the smaller the mortgage. That part is obvious. What is less obvious is how that choice ripples through everything else.

With 3% down, you may qualify sooner because you need less cash upfront. That can be a lifesaver in an expensive market. But your monthly payment will be higher because you are borrowing more, and you will likely owe mortgage insurance. With 20% down, you avoid conventional PMI and reduce your loan balance substantially, but you may tie up so much cash that you have little left for repairs, moving costs, furniture, or an emergency fund.

Buying a home without a financial cushion is one of those situations that feels responsible for about 48 hours, right until the water heater dies, the HVAC starts making horror-movie noises, and you discover the seller’s idea of “updated electrical” was more of a creative writing exercise.

Do You Really Need 20% Down?

No. Let’s say that clearly for the people in the back and for anyone still being lectured by a relative who bought a house in 1997 for the price of a modern parking spot.

You do not need 20% down to buy a home in many cases. That number matters mainly because it is the threshold where conventional borrowers can usually avoid PMI. It is an important benchmark, but it is not a mandatory entry ticket.

Many buyers, especially first-time homebuyers, put down much less. That is one reason low-down-payment loan programs exist. They are designed to help qualified buyers get into homes sooner, rather than forcing them to spend years chasing a savings target that keeps running away as home prices rise.

Common Home Loan Down Payment Ranges

Conventional Loans

Some conventional loans allow qualified buyers to put down as little as 3%. These programs can be appealing if you have solid credit and want a lower upfront requirement. The tradeoff is usually PMI when your down payment is under 20%.

FHA Loans

FHA loans are often popular with first-time buyers and buyers with less-than-perfect credit. They can offer a lower barrier to entry, but they come with mortgage insurance rules that may be more persistent than conventional PMI. In other words, FHA can help you get in the door, but the monthly cost structure deserves a close look.

VA Loans

Eligible borrowers using VA loans may be able to buy with no down payment. That is a huge advantage. These loans also do not require monthly mortgage insurance, though there may be an upfront funding fee depending on your situation.

USDA Loans

Qualified buyers in eligible rural areas may also be able to purchase with no down payment through USDA-backed financing. These loans can be fantastic for the right borrower, especially if location and income guidelines line up.

Jumbo Loans

If you are buying in a higher price range, jumbo loan rules can be stricter. Many lenders want larger down payments here because the loan amount itself makes them sweat a little.

How Much Should You Put Down?

The answer is not “as much as humanly possible.” The answer is “enough to improve your loan terms without wrecking your broader financial life.”

3% to 5% Down

This range can make sense if:

You want to buy sooner rather than later, have steady income, decent credit, and enough savings left after closing to handle repairs and emergencies. It can also be a good strategy if waiting for 20% would keep you renting for years in a market where prices are still pushing upward.

The downside is obvious: bigger loan, higher payment, and likely mortgage insurance.

10% Down

For many buyers, 10% is the sweet spot. It is large enough to reduce the loan balance meaningfully, often improve pricing, and shrink mortgage insurance costs compared with a minimal down payment. At the same time, it may still leave room for reserves.

If 20% feels like a financial marathon but 3% feels too skinny, 10% is often the practical middle road.

20% Down

This is the classic target because it can eliminate PMI on conventional loans and lower your monthly payment. It also gives you stronger equity on day one. If you can comfortably do it and still keep emergency savings, retirement contributions, and moving funds intact, great.

If getting to 20% means emptying every account and living on hope, caffeine, and unplanned overtime, it may not be the smartest move after all.

What Else You Need Besides the Down Payment

A lot of buyers focus so hard on the down payment that they forget about the rest of the cash needed to close the deal. That is how people end up shocked by numbers that were technically disclosed but emotionally ignored.

Beyond the down payment, you may need money for:

Closing costs, lender fees, appraisal fees, title charges, prepaid taxes and insurance, moving expenses, utility setup, and immediate home fixes. In many markets, closing costs alone can land in the 2% to 5% range of the purchase price.

That means on a $400,000 home, a buyer aiming for 10% down might need far more than $40,000 available. If closing costs come in near 3%, that is another $12,000, before the moving truck even shows up.

When a Larger Down Payment Makes Sense

You may want to put more down if:

You need to lower your monthly housing cost to fit your budget. You want to reduce how much interest you will pay over time. You want to avoid PMI. You are buying in a competitive market where a stronger financial profile can make your offer more attractive. Or you simply sleep better knowing you owe less money. Financial peace has value too.

A larger down payment can also help buyers who are close to lender qualification limits. Reducing the loan amount may improve debt-to-income math and help a file go from “maybe” to “approved.”

When a Smaller Down Payment Might Be Smarter

Yes, sometimes the better move is putting less down. That sounds rebellious, but it is often just practical.

A smaller down payment may make sense if:

You would otherwise wipe out your emergency fund. You need cash left over for repairs or renovations. You have high-interest debt that should be handled first. You can qualify for a strong loan program with a low-down-payment option. Or you are prioritizing liquidity because life has a habit of sending invoices without notice.

Money trapped in your home is not as flexible as money sitting in savings. Home equity is useful, but it is not the same thing as accessible cash.

How to Choose the Right Number for You

Start with your total available cash, then subtract what you need for closing costs, moving expenses, repairs, and an emergency cushion. What remains is the true amount you can put down without leaving yourself financially brittle.

Then compare loan scenarios. Ask lenders to show you the monthly payment, mortgage insurance cost, rate, and cash-to-close numbers at different down payment levels. Compare 5%, 10%, and 20% side by side. Numbers have a wonderful way of clearing out myths, family folklore, and overconfident internet advice.

You should also ask about down payment assistance, grants, gift funds, and special loan products. Many buyers assume they have to do everything alone, when in reality there may be programs that help reduce the upfront burden.

Down Payments on Cars Work the Same Basic Way

Homes get most of the down-payment attention, but the same principle applies to auto loans. A down payment on a car lowers the amount you need to finance and can sometimes improve your interest rate. It can also reduce the risk of ending up upside down on the loan, where you owe more than the car is worth. That is not a fun place to be, especially when the car is already depreciating like it has somewhere else to be.

Common Down Payment Mistakes to Avoid

Confusing Down Payment With Cash to Close

Your down payment is only part of the upfront cost. If you ignore the rest, you may end up house hunting with half a budget.

Draining Every Dollar You Have

A beautiful closing day becomes less beautiful when you own a home but cannot afford the first surprise repair.

Obsessing Over 20% at the Expense of Timing

Waiting for a perfect number can backfire if prices rise, rates change, or your rent keeps climbing while you save.

Choosing Based Only on Monthly Payment

Lower monthly payments are nice, but do not ignore your remaining savings, total loan cost, or future flexibility.

Not Comparing Loan Types

Sometimes a lower-down-payment loan is actually the better overall deal. Sometimes it is not. Compare the whole package, not just the headline percentage.

Real-World Experiences and Lessons From Buyers

One buyer saved aggressively for years, determined to hit 20% down because that seemed like the gold standard. By the time they got there, they had almost no extra cash left. They bought the house, skipped PMI, and felt triumphant for exactly one month. Then the roof needed repair, the fridge failed, and a plumbing issue appeared like an uninvited sequel. Their biggest lesson was that being “house rich” on paper and cash poor in real life is not a winning combination.

Another buyer went the opposite direction and put 5% down on a conventional loan. At first, the idea of paying PMI irritated them on a spiritual level. But keeping extra money in the bank turned out to be the smarter move. They used those reserves for paint, flooring, and a minor bathroom update that made the home far more livable. A couple of years later, with more equity built and finances still intact, the earlier PMI payments felt less like a tragedy and more like the cost of getting into the market sooner.

A first-time buyer using an FHA loan loved the lower barrier to entry but admitted they had not fully appreciated how mortgage insurance would affect the monthly payment over time. Their advice to future buyers was simple: do not just ask, “Can I qualify?” Ask, “Will this still feel comfortable six months after closing when the novelty wears off and the bills become normal?” That is a better question.

A military family using a VA loan had one huge advantage: no down payment requirement. That gave them flexibility to keep savings for moving costs, furniture, and the unpredictable chaos that often comes with relocation. Their takeaway was that zero down is not automatically reckless. For the right borrower and the right program, it can be a smart use of benefits rather than a shortcut.

There was also the buyer who became obsessed with shaving every possible dollar off the monthly payment. They considered throwing nearly all their cash into the down payment. Then they ran multiple loan estimates and realized that putting slightly less down would still keep the payment manageable while preserving a healthy emergency fund. They later said that decision gave them more confidence than any perfect-looking spreadsheet ever could.

One of the most common emotional experiences buyers describe is the strange guilt of not reaching 20%. People feel like they are somehow doing homeownership incorrectly. But home buying is not a purity test. It is a math problem mixed with life goals. If 8% down gets you into a stable home while preserving your emergency savings, that may be a stronger decision than forcing yourself to 20% and spending the next year panicking every time the HVAC coughs.

Another recurring lesson is that buyers often underestimate how different the house feels after closing. Before closing, the down payment is the star of the show. After closing, what matters most is whether the payment is sustainable, whether you still have cash, and whether your home supports your real life instead of just your fantasy life. That is why the best down payment is rarely the biggest one you can scrape together. It is the one that helps you buy the home and keep living like a functional adult afterward.

Final Thoughts

Down payments matter, but they are not about winning a contest for who can hand over the biggest pile of cash. They are about balancing affordability, risk, flexibility, and long-term goals. A larger down payment can lower your costs and strengthen your position. A smaller one can get you into the market sooner and preserve much-needed savings. Both can be smart. Both can be foolish. Context is everything.

If you remember one thing, let it be this: the best down payment is the amount that gets you into the right home with a payment you can handle, while leaving enough money for the rest of your actual life. Because owning a home is great, but owning a home and still being able to sleep at night is even better.