Table of Contents >> Show >> Hide

- The quick answer: a 3% mortgage can be worth tens (or hundreds) of thousands

- Two ways to measure “how much it’s worth”

- The “same payment” test: how much more house does 3% buy?

- Why 3% feels like a golden handcuff (and sometimes it is)

- Can you sell the house and keep the 3% mortgage?

- Assumable mortgages: the rare case where 3% can be “portable”

- Discount points and buy-downs: can you “buy” your way back to 3%?

- Refinancing: is a 3% mortgage ever worth refinancing?

- Decision framework: what should you do with your 3% mortgage?

- Common misconceptions (aka, things that cause group-text arguments)

- Real-world experiences: what people learn about a 3% mortgage (the 500-word reality section)

- Conclusion: the real value of 3% is what it lets you do

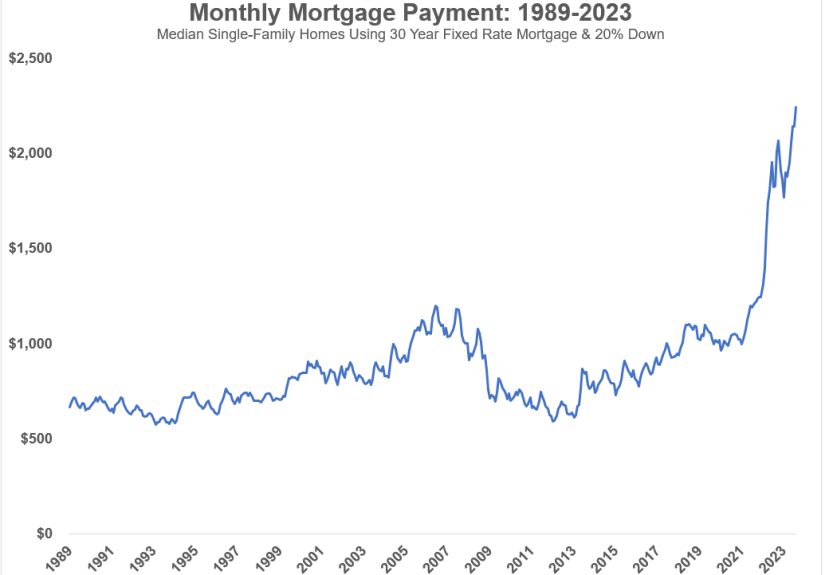

A 3% mortgage is the financial equivalent of finding an original Pokémon card in the pocket of a winter coat you haven’t worn since 2021: you’re thrilled, you’re slightly suspicious, and you immediately want to put it in a protective sleeve. In a world where “normal” rates have been hanging out much higher, a 3% note can feel like a superpower. But how much is it actually worthin dollars, in choices, and in peace of mind?

Let’s put real math on the feelings. We’ll compare payments, total interest, and “rate-lock” tradeoffs, then translate it all into practical decisions: keep the house, move anyway, refinance (maybe), orif you’re luckytransfer that magical rate through an assumable loan.

The quick answer: a 3% mortgage can be worth tens (or hundreds) of thousands

“Worth” depends on three things: (1) your loan balance, (2) the rate you’d get today, and (3) how long you’ll keep paying on the loan. The bigger the balance and the longer you keep it, the more valuable that low rate becomes.

A concrete example (principal + interest only)

Suppose you have (or want) a $400,000 30-year fixed mortgage. Here’s what the monthly principal-and-interest payment looks like:

| Rate | Monthly Payment (P&I) | Total Interest Over 30 Years |

|---|---|---|

| 3.00% | $1,686 | $207,110 |

| 6.00% | $2,398 | $463,353 |

| 7.00% | $2,661 | $558,036 |

Translation: compared with a 6% loan on the same balance, a 3% mortgage saves about $712 per month. Compared with 7%, it saves about $975 per month. Over 30 years, the total interest difference can be massiveroughly $256,000 saved versus 6%, or about $351,000 versus 7%. (Taxes, insurance, HOA, and mortgage insurance are separate line itemsstill important, just not part of this interest-rate math.)

Two ways to measure “how much it’s worth”

1) The monthly-cash-flow value

If a low rate reduces your monthly payment, it increases your flexibility. That flexibility has value even if you don’t plan to keep the loan for 30 years. A 3% mortgage can mean:

- More breathing room for childcare, student loans, or just groceries doing their own little inflation dance.

- More capacity to invest (retirement, emergency fund) instead of sending money to Interest Land, population: everybody with a high rate.

- More resilience if income changesbecause your housing payment is less likely to become the villain in your budget.

2) The “mortgage-as-an-asset” value (present value of savings)

Think of the rate difference like a discount you’re receiving every month. The “asset value” is the present value of those payment savings compared with what you’d pay at a higher rate.

Example: If your 3% payment is $712/month lower than a 6% alternative on a $400,000 balance, that’s $8,544/year in savings. If you keep the loan for 10 years, you’re looking at roughly $85,000 in raw payment differencebefore considering how the loan amortizes, what you could earn by investing the difference, and what inflation does over time.

The key idea: the value is front-loaded in your decision-making. You don’t need to keep the mortgage for 30 years for it to be meaningful; even a handful of years can represent serious money.

The “same payment” test: how much more house does 3% buy?

Here’s the sneaky power of low rates: they don’t just lower the paymentthey increase how much you can borrow for the same monthly cost.

Using the earlier example, the $2,398/month payment (what $400,000 costs at 6%) could support roughly $569,000 at 3% on a 30-year term. That’s about $169,000 more borrowing power at the same monthly payment.

This is one reason 3% mortgages feel “sticky.” When rates rise, moving to a new place can mean paying more each month even if the home price is similar or downsizing and still not saving as much as you’d expect.

Why 3% feels like a golden handcuff (and sometimes it is)

The phrase “rate lock-in” exists for a reason: when you hold a much lower rate than the market, you have a built-in disincentive to sell. It’s not just emotional; it’s mathematical.

When keeping the 3% loan is almost always the better deal

- You’re happy in the home (location, schools, commute, neighbors who don’t run leaf blowers at sunrise).

- You expect to stay put at least 3–5 years and have no urgent life reason to move.

- Your payment is comfortable and you’re not stretching to maintain it.

- You have other high-interest debt you could eliminate faster because the mortgage isn’t draining you.

When moving can still make senseeven with a 3% mortgage

A low rate is powerful, but it’s not your landlord. If the house no longer fits your life, a mortgage rate shouldn’t be the only voice in the room. Moving can be rational if:

- Your income has grown and the lifestyle benefit outweighs the extra interest cost.

- You need space or accessibility (new baby, multigenerational living, health needs).

- You’re relocating for work or familyand the alternative is commuting from another time zone.

- The home is expensive to maintain (big repairs) and a different property reduces long-term risk.

The right question isn’t “Should I ever give up 3%?” It’s: How much does my next-best option cost me, and what do I get in return?

Can you sell the house and keep the 3% mortgage?

Usually, no. Most mortgages aren’t designed to be casually transferred to a new buyer like a streaming password (and lenders are way less fun at parties). Many loans include rules that require payoff when the home is sold. That’s why assumable mortgages matter so much.

Assumable mortgages: the rare case where 3% can be “portable”

If a mortgage is assumable, a qualified buyer may be able to take over the seller’s loan balance, rate, and remaining term. This is most commonly associated with certain government-backed loans (like FHA and VA), not typical conventional loans.

Why assumption can add real resale value

If you’re selling a home with an assumable 3% mortgage, you’re not just selling a kitchen and a backyardyou’re selling a payment. That payment can be dramatically lower than what a buyer would get with a new loan at today’s rates, so buyers may be willing to:

- Pay a higher purchase price,

- Compete harder (fewer seller concessions demanded), or

- Move faster to lock in the assumption opportunity.

The catch: the buyer may need cash (or a second loan)

Most assumptions cover the remaining loan balancenot the full purchase price. If you owe $320,000 at 3% but the home sells for $500,000, the buyer needs to cover the $180,000 gap. That can happen via:

- Cash down payment,

- A second mortgage/HELOC (often at higher rates), or

- Other financing arrangements (which can complicate the deal).

So the “value” of an assumable 3% mortgage is still huge, but it may be limited to buyers who can bridge the gap. In practice, that can narrow the buyer poolwhile making those buyers extremely interested.

Discount points and buy-downs: can you “buy” your way back to 3%?

Sometimes you’ll hear: “Just buy points.” Points are prepaid interest that can reduce your rate, but the size of the reduction varies. The most important concept is the break-even point: how long you must keep the mortgage for the upfront cost to pay off.

The break-even formula (easy enough to do on a napkin)

Break-even months = Cost of points ÷ Monthly payment savings

Example: If points cost $6,000 and save you $150/month, break-even is 40 months (about 3.3 years). If you refinance or sell before then, you didn’t really “save”you just prepaid.

Important reality check: buying down from something like 6% all the way to 3% is usually not a normal points scenario. That kind of drop would likely require a very large upfront cost (if it’s even available), and lenders’ pricing changes daily. So points are best viewed as a tool for small improvementstightening the rate a bitnot time-traveling back to peak low-rate era.

Refinancing: is a 3% mortgage ever worth refinancing?

People do refinance 3% loans, but it’s rarely because a lower rate is available. It’s usually because they want a different structure:

- Cash-out refinance for renovations or debt consolidation (often risky if it replaces cheap debt with expensive debt later).

- Term change (e.g., switching to a shorter term to pay off fasterthough you can often do that by paying extra instead).

- Removing mortgage insurance in special cases (sometimes possible without refinancing, depending on the loan type and equity).

If your goal is “pay less interest,” a 3% mortgage is already doing that job extremely well. Many homeowners choose to keep the 3% note and: (1) make extra principal payments when they can, and (2) invest the difference versus what a higher-rate loan would cost.

Decision framework: what should you do with your 3% mortgage?

Here are practical rules that keep the math honest without pretending your life is a spreadsheet.

Rule 1: Separate “house choice” from “loan choice”

Ask two different questions: (A) Do I want to live in this home for the next 3–7 years? (B) If I didn’t already have this mortgage, would I choose it today? If the answer to (A) is “yes,” your 3% mortgage is likely a keeper. If (A) is “no,” don’t let the rate trap you in a home that doesn’t fit.

Rule 2: Price the move in monthly dollars first, not headlines

When comparing staying vs. moving, focus on monthly payment difference (including property taxes, insurance, HOA, and any mortgage insurance). A higher rate hurts most through cash flow. If moving increases your monthly outlay by $700–$1,000, that’s not abstractit’s a car payment.

Rule 3: Treat points and buy-downs like a “time-in-home bet”

If you’re paying extra upfront to reduce the rate (points or a temporary buydown), you’re betting you’ll keep the mortgage long enough to break even. Shorter stay? Consider keeping cash instead.

Rule 4: If assumption is on the table, do the gap math early

If your loan is assumable, your 3% mortgage can become a selling feature. But the buyer’s ability to cover the price-to-balance gap is critical. Sellers: understand your payoff balance and likely sales price. Buyers: know how you’ll fund the gap, and don’t assume “assumable” means “no cash needed.”

Common misconceptions (aka, things that cause group-text arguments)

“A 3% mortgage is always better than paying cash.”

Often, cheap debt is attractivebut “always” is too strong. Paying cash reduces risk and monthly obligations. The best answer depends on your emergency fund, retirement savings, risk tolerance, and whether “cash buyer” status wins you a better deal.

“If rates drop, I’ll just refinance later.”

Maybebut refinancing isn’t free. Closing costs, appraisal requirements, and lender pricing all matter. A refinance only works if the new payment savings outweigh costs within your time horizon.

“My 3% mortgage is worth the same amount to everyone.”

Not quite. The value is higher to someone who: stays longer, has a larger balance, and would otherwise borrow at a higher rate. It can also be more valuable in markets where prices are high and buyers are payment-sensitive.

Real-world experiences: what people learn about a 3% mortgage (the 500-word reality section)

Ask homeowners who locked in around 3%, and you’ll hear a pattern: at first it feels like “nice timing,” and later it feels like a defining feature of their financial life. Many describe it as a quiet advantage that shows up every month, the way good sleep shows up in your moodsubtle, consistent, and hard to give up once you’ve had it.

One common experience is the “moving day math spiral.” People start browsing listings for fun, then they run payment estimates and suddenly feel like the internet has personally attacked them. It’s not that the new house is wildly more expensiveit’s that the interest rate changes the entire shape of the payment. Homeowners often report that this realization reframes what they even want from a move: instead of “bigger,” it becomes “better layout,” “closer to work,” or “one less bathroom to clean,” because the payment jump makes “more house” feel less appealing.

Another recurring lesson is that a low mortgage rate can encourage smarter (and sometimes sneakier) financial behavior. Some homeowners take the monthly savings and automatically funnel it into retirement accounts. Others use it to pay off higher-interest debt faster, effectively upgrading their overall balance sheet without changing anything about their house. The surprising part is how often people say this strategy felt easier than expectedbecause the money never sat around long enough to get spent on “tiny treats” that somehow add up to a second mortgage in snack form.

There’s also the “renovate vs. relocate” pivot. With a 3% mortgage, homeowners frequently explore remodeling to solve space or function problems: finishing a basement, adding built-ins, converting a dining room into an office, or upgrading insulation and HVAC for comfort. The logic is simple: improving the current home can be cheaper than replacing a 3% loan with a much higher-rate loan. The emotional bonus is real toopeople like feeling like they outsmarted the market, even if the market was just doing market things.

Finally, people with assumable loans often describe an “aha” moment when they realize the rate itself can be part of the home’s appeal. Sellers learn that showcasing a low-rate assumption opportunity (when applicable) can attract buyers who are payment-focused, not just price-focused. Buyers learn the flip side: the assumption is powerful, but the cash needed to bridge the gap can be the real hurdle. Those who successfully assume a low-rate mortgage often describe it as one of the most impactful financial decisions they’ve madebecause it changes the monthly reality of homeownership, not just the story they tell themselves about it.

The big takeaway from these lived patterns: a 3% mortgage isn’t only “worth” a number. It’s worth optionsthe ability to stay flexible, save aggressively, absorb surprises, and choose your next move on your timeline. If you treat it like a tool instead of a trophy, it can keep paying you back long after the excitement of the rate lock wears off.

Conclusion: the real value of 3% is what it lets you do

A 3% mortgage can be worth a startling amount of money in reduced monthly payments and long-run interestespecially on larger balances. But its most practical value is simpler: it buys flexibility. It can make staying put cheaper, moving more expensive, and remodeling more attractive. If your loan is assumable, it can even become a selling advantagethough the buyer’s ability to cover the price gap matters.

If you want the cleanest way to answer “How much is it worth?” do this: compare your current payment to the payment you’d get at a realistic market rate on your remaining balance, then multiply the monthly difference by how long you expect to keep the loan. That number won’t capture every nuance, but it will capture the part that hits your bank account every monthwhich is, conveniently, the part that tends to matter.