Table of Contents >> Show >> Hide

- What Is Capitalization Rate in Real Estate?

- Why Investors Use Cap Rate to Calculate Property Value

- The 3-Step Process to Calculate Property Value With Capitalization Rate

- Example 1: Valuing a Small Apartment Building

- Example 2: Same NOI, Different Cap Rate, Very Different Value

- Example 3: Reverse-Engineering the NOI You Need

- How to Choose a Realistic Cap Rate

- Common Mistakes When Using Cap Rate to Value Property

- Cap Rate vs. Other Real Estate Metrics

- When the Capitalization Rate Method Works Best

- A Simple Checklist Before You Trust Your Valuation

- Final Thoughts on How to Calculate Property Value With Capitalization Rate

- Real-World Experience: What Investors Learn After Using Cap Rate in the Wild

- SEO Tags

If you have ever looked at an investment property and thought, “This place seems promising, but is it actually worth the asking price?” congratulations: you are already asking the right question. In real estate investing, charm is nice, granite countertops are nice, and a suspiciously enthusiastic listing description is… well, entertaining. But none of those things tell you what an income-producing property is really worth.

That is where the capitalization rate, usually called the cap rate, comes in. It is one of the most popular shortcuts in commercial real estate and rental property analysis because it helps investors connect a property’s income to its market value. In plain English, cap rate helps answer this question: Based on the income this property produces, what should it be worth?

In this guide, you will learn how to calculate property value with capitalization rate, how to calculate net operating income correctly, how to choose a realistic cap rate, and how to avoid the classic mistakes that make smart people accidentally pay “luxury pricing” for “needs everything.” We will also walk through specific examples so the math feels less like a finance exam and more like something you can actually use.

What Is Capitalization Rate in Real Estate?

The capitalization rate is the relationship between a property’s net operating income (NOI) and its value. Investors use it to estimate the unlevered return on a property over a one-year period. “Unlevered” is just a fancy way of saying before financing enters the chat. In other words, cap rate looks at the property itself, not the mortgage you may or may not use to buy it.

Here is the basic formula:

Cap Rate = Net Operating Income ÷ Property Value

If you already know the NOI and the cap rate, you can flip the formula to estimate value:

Property Value = Net Operating Income ÷ Cap Rate

That second formula is the star of this article. It is the heart of the income capitalization approach and one of the fastest ways to estimate what an income-producing property may be worth in the market.

Why Investors Use Cap Rate to Calculate Property Value

Cap rate is popular because it is quick, practical, and surprisingly useful when you are comparing similar properties. If two apartment buildings are in similar neighborhoods and have similar risk profiles, cap rate gives you a fast way to see whether one is overpriced, underpriced, or wearing an unjustified confidence blazer.

It is especially helpful for:

- Apartment buildings

- Single-family rentals

- Small multifamily properties

- Retail centers

- Office properties

- Industrial buildings

- Other income-producing real estate

It is less helpful for owner-occupied homes, fix-and-flip projects, vacant land, or properties with wildly unstable income. A cap rate formula is only as useful as the income stream behind it.

The 3-Step Process to Calculate Property Value With Capitalization Rate

Step 1: Calculate Net Operating Income (NOI)

Before you can value a property using cap rate, you need the NOI. This is the annual income the property generates after operating expenses, but before mortgage payments, income taxes, depreciation, and major capital expenditures.

NOI Formula:

Gross Rental Income + Other Income − Vacancy Loss − Operating Expenses = NOI

Let’s break that down.

Income That Usually Counts Toward NOI

- Annual rent collected

- Parking income

- Laundry income

- Pet fees or storage fees

- Other recurring property income

Expenses That Usually Count Against NOI

- Property taxes

- Insurance

- Repairs and maintenance

- Property management fees

- Utilities paid by the owner

- Landscaping and janitorial costs

- Administrative costs

- Advertising and leasing expenses

- Routine service contracts

Items That Usually Do Not Go Into NOI

- Mortgage principal and interest

- Income taxes

- Depreciation

- Capital improvements such as a new roof, full renovation, or building addition

This is where people often make a mess of the math. If you subtract your loan payment when calculating NOI, you are no longer measuring the property’s operating performance. You are mixing property analysis with financing decisions, and that turns your “clean valuation” into a spreadsheet casserole.

Step 2: Find the Appropriate Market Cap Rate

Once you know the NOI, you need a realistic cap rate. This is not a number you invent because 5.5% “feels classy.” It should come from the market.

The best way to estimate cap rate is to look at comparable properties in the same market with similar:

- Property type

- Location

- Age and condition

- Occupancy level

- Tenant quality

- Lease structure

- Risk profile

Generally speaking, lower cap rates are associated with properties that investors see as lower risk, more stable, or located in stronger markets. Higher cap rates often reflect more perceived risk, more management intensity, weaker locations, shorter leases, or uncertainty around income.

And here is the key relationship to remember:

Lower cap rate = Higher property value

Higher cap rate = Lower property value

That inverse relationship is the whole game. Small changes in cap rate can create very large changes in value.

Step 3: Apply the Formula

Once you have NOI and a market-supported cap rate, the formula is easy:

Property Value = NOI ÷ Cap Rate

Make sure the cap rate is written as a decimal in the calculation. So:

- 5% = 0.05

- 6.5% = 0.065

- 8% = 0.08

Example 1: Valuing a Small Apartment Building

Suppose a four-unit rental property generates:

- Gross annual rent: $96,000

- Other income: $4,000

- Vacancy allowance: $5,000

- Operating expenses: $35,000

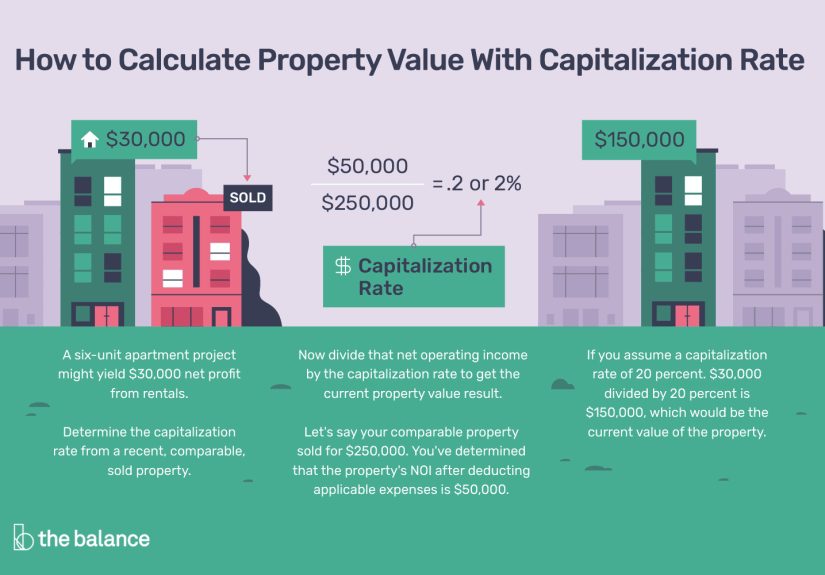

NOI = $96,000 + $4,000 − $5,000 − $35,000 = $60,000

Now let’s say similar small multifamily properties in that market are trading around a 6% cap rate.

Property Value = $60,000 ÷ 0.06 = $1,000,000

So based on the capitalization rate method, the estimated property value is $1 million.

If the seller is asking $1.2 million, you may want to ask whether the building comes with a hidden gold mine, a celebrity tenant, or just optimism.

Example 2: Same NOI, Different Cap Rate, Very Different Value

Let’s keep the NOI at $60,000, but change the cap rate.

- At a 5% cap rate: $60,000 ÷ 0.05 = $1,200,000

- At a 6% cap rate: $60,000 ÷ 0.06 = $1,000,000

- At a 7% cap rate: $60,000 ÷ 0.07 = $857,143

Same property income. Three very different values. That is why choosing the right cap rate matters so much. A one-point shift can swing value by hundreds of thousands of dollars.

Example 3: Reverse-Engineering the NOI You Need

Sometimes investors know the target purchase price and the market cap rate, but want to figure out the NOI the property should produce.

Suppose you want to buy a property for $850,000 in a market where similar properties trade around a 6.8% cap rate.

Required NOI = Property Value × Cap Rate

Required NOI = $850,000 × 0.068 = $57,800

That means the property should produce about $57,800 in annual NOI to support that price at that cap rate. If the actual NOI is far lower, the asking price may be too high.

How to Choose a Realistic Cap Rate

This is the part where real-world investing separates itself from internet bravado. You cannot value a property accurately if your cap rate is based on wishful thinking. The strongest cap-rate analysis comes from verified comparable sales, broker opinions, appraiser reports, market surveys, and local investor knowledge.

When selecting a cap rate, consider:

- Location: Stronger locations often command lower cap rates.

- Asset class: Multifamily, industrial, office, and retail properties can all trade differently.

- Tenant strength: Stable tenants can support lower cap rates.

- Lease term: Long leases often reduce uncertainty.

- Condition: Deferred maintenance may push cap rates higher.

- Vacancy and collections: Unstable income raises risk.

- Market conditions: Interest rates, liquidity, and demand all influence cap rates.

If you are new to investing, resist the urge to grab a generic “good cap rate” from the internet and apply it everywhere. A cap rate that looks reasonable for a stabilized apartment building in one city may be nonsense for a value-add retail strip in another.

Common Mistakes When Using Cap Rate to Value Property

1. Using Gross Rent Instead of NOI

Gross rent is not NOI. If you forget expenses, you will overvalue the property and possibly volunteer to become the proud owner of a financial headache.

2. Ignoring Vacancy

Even great properties have turnover, nonpayment risk, or downtime between tenants. Pretending vacancy is zero forever is not analysis. It is fan fiction.

3. Mixing Debt Service Into NOI

Mortgage payments do not belong in NOI. Cap rate is designed to evaluate the property’s income independent of financing.

4. Choosing a Cap Rate With No Market Support

If you pick a cap rate just because it helps justify your offer, you are not discovering value. You are role-playing as an appraiser.

5. Using One-Time Expenses or One-Time Income Incorrectly

A one-off plumbing disaster or a temporary rent spike should not automatically define stabilized NOI. The point is to estimate normal annual operations.

6. Applying Cap Rate to the Wrong Property Type

Cap rate works best for income-producing properties with reasonably stable operations. It is less reliable for vacant buildings, heavy repositioning deals, or owner-user properties.

Cap Rate vs. Other Real Estate Metrics

Cap rate is important, but it is not the only number worth knowing.

Cap Rate vs. Cash-on-Cash Return

Cap rate ignores financing. Cash-on-cash return includes the actual cash invested and the impact of the mortgage. If you want to know how hard your cash is working, cash-on-cash matters.

Cap Rate vs. Gross Rent Multiplier

Gross rent multiplier is faster, but much rougher. It does not account for expenses. Cap rate is more informative because it focuses on net operating income.

Cap Rate vs. Discounted Cash Flow

DCF is more detailed because it models cash flows over multiple years and includes a resale assumption. Cap rate is simpler and quicker. Think of cap rate as the sharp pocketknife and DCF as the full toolbox.

When the Capitalization Rate Method Works Best

The cap rate approach is most useful when the property has:

- Stable or predictable income

- Reliable operating history

- Comparable local sales data

- Market rents that can be reasonably estimated

It is especially handy for initial screening. Investors often use it early in the process to decide whether a property deserves deeper underwriting.

But it should not be the only tool in your kit. A property can show a nice cap rate and still be a weak investment if it has hidden repairs, bad leases, poor demographics, or a financing structure that crushes cash flow.

A Simple Checklist Before You Trust Your Valuation

- Have you used annualized, realistic income?

- Did you include vacancy and credit loss?

- Did you subtract normal operating expenses?

- Did you exclude mortgage payments and capital improvements?

- Did you use a market-supported cap rate from comparable assets?

- Did you stress test the value at slightly higher and lower cap rates?

If you can say yes to all of those, your valuation is probably on much firmer ground.

Final Thoughts on How to Calculate Property Value With Capitalization Rate

If you remember only one formula from this article, make it this one: Property Value = NOI ÷ Cap Rate. That single equation explains a huge portion of how income-producing real estate is priced.

The beauty of the cap rate method is that it forces you to focus on what actually matters: the property’s income, the cost to operate it, and the market’s required return for that level of risk. It cuts through glossy listings, dramatic staging, and the timeless seller argument that “this area is really up-and-coming.” Maybe it is. Maybe it is just up-and-chatting.

Used correctly, capitalization rate is a powerful way to estimate real estate value. Used carelessly, it can turn a decent deal into an overpriced lesson. So run the numbers carefully, verify your assumptions, compare similar properties, and let the math do the talking. It is a lot less emotional than a listing agent, and usually much better at arithmetic.

Real-World Experience: What Investors Learn After Using Cap Rate in the Wild

On paper, cap rate valuation looks beautifully neat. You gather the income, subtract the operating expenses, divide by the market cap rate, and out pops a value. In the real world, though, the lesson most investors learn quickly is that the formula is simple, but the inputs are where the battle happens.

One common experience is discovering that seller-provided numbers are often “aspirational.” The rent roll may look strong, but then you find out one tenant is two months behind, one unit has been “temporarily vacant” since the invention of streaming television, and the maintenance budget appears to have been calculated using hope instead of invoices. The first time an investor compares advertised NOI with normalized NOI, the difference can be eye-opening. Suddenly, the amazing deal starts looking like a very polite ambush.

Another real-world lesson is how sensitive value is to cap rate movement. New investors are often shocked that a tiny shift in cap rate can dramatically change a property’s price. That feels theoretical until you are in a competitive market where buyers accept a lower cap rate for a cleaner building in a stronger neighborhood. Then it becomes very real. The property did not magically produce more income overnight; the market simply priced the risk differently.

Experienced investors also learn that cap rate works best when paired with judgment. A property with a higher cap rate is not automatically better. Sometimes it is higher because the location is weaker, the tenants are shaky, or future expenses are lurking around the corner wearing steel-toe boots. On the other hand, a lower cap rate can still make sense if the area is growing, the property is well maintained, and the income stream is durable.

Many investors say their best decisions came after adjusting NOI for the real world: raising vacancy assumptions, plugging in realistic repairs, and budgeting for management even if they plan to self-manage. Why? Because time has value, roofs age whether you acknowledge them or not, and “I’ll handle everything myself forever” is not an investment strategy. It is a motivational poster.

Perhaps the biggest experience-based takeaway is this: cap rate is not magic, but it is incredibly useful. It gives investors a fast way to translate income into value, compare deals, and spot red flags early. The people who use it well are not the ones who memorize the formula. They are the ones who respect the assumptions behind it.