Table of Contents >> Show >> Hide

- What “Chaotic Markets” Actually Means (and Why It Feels So Personal)

- The Core Rules That Keep You Alive (Financially) When Markets Go Wild

- 1) Build a “Do Not Touch” Cash Buffer (So You Don’t Sell at the Worst Time)

- 2) Use Asset Allocation Like a Seatbelt, Not a Vibe

- 3) Diversify Like You Mean It (Because Eggs Hate One Basket)

- 4) Automate Investing to Outrun Your Emotions

- 5) Rebalance: The Grown-Up Way to “Buy Low, Sell High”

- 6) Keep Costs Low (Because Fees Don’t Care About Your Feelings)

- 7) Use Tax Moves Carefully (If They Apply), and Don’t Step on the Wash-Sale Rake

- 8) Beware of “Volatility Season” Scams and Too-Good-To-Be-True Promises

- A Survival Checklist for the Next Time the Market Throws a Tantrum

- Specific Examples: What “Staying the Course” Looks Like in Real Life

- How to Know If Your Plan Is Too Risky (Before Chaos Exposes It)

- Market Mechanics You Should Know (So You Don’t Panic Over Normal Stuff)

- What Not to Do in Chaotic Markets (A Short Comedy in Three Acts)

- When to Get Help

- Experiences From Chaotic Markets: 10 Lessons People Learn the Hard Way (About )

- Conclusion

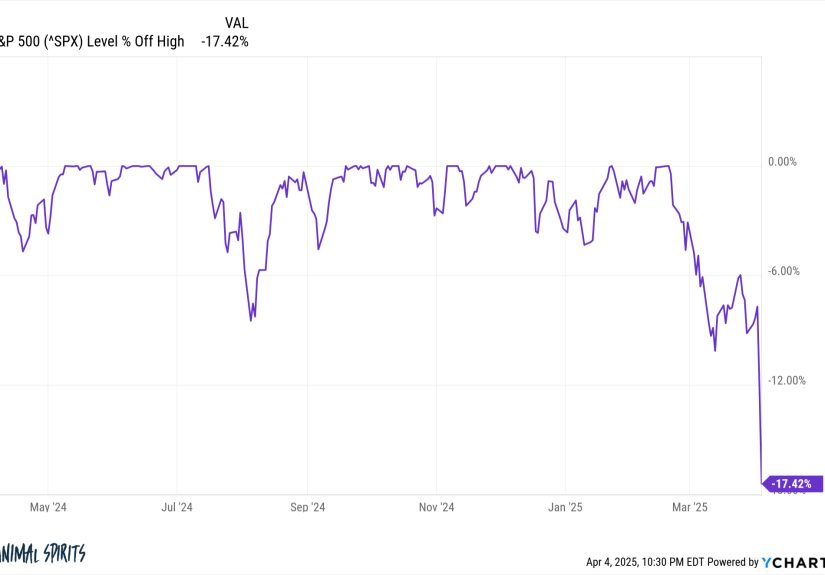

Chaotic markets are like a toddler with a drum set: loud, unpredictable, and weirdly confident. One day your portfolio is doing a victory lap.

The next day it’s face-planting in slow motion while financial headlines scream in all caps. The good news? You don’t need superpowers to

survive volatility. You need a plan that’s boring on purpose, plus a few practical habits that keep you from making expensive decisions

during emotionally spicy moments.

This guide is educational (not personal investment advice). If you’re investing as a teen, it’s smart to involve a parent/guardian and, if possible,

a licensed financial professionalespecially before making big moves.

What “Chaotic Markets” Actually Means (and Why It Feels So Personal)

“Chaotic” usually means prices are swinging fast, uncertainty is high, and the market can’t decide whether it’s optimistic or panicking.

Volatility often spikes around inflation surprises, interest-rate shifts, geopolitical events, earnings shocks, or simply the market having

an existential crisis before lunch.

Here’s the sneaky part: volatility isn’t just a math conceptit’s a feelings concept. Big drops can trigger loss aversion (pain of losing feels

stronger than joy of winning), recency bias (assuming what’s happening now will keep happening), and headline hypnosis (believing whatever

the loudest alert says). Surviving chaos is mostly about building guardrails for your own brain.

The Core Rules That Keep You Alive (Financially) When Markets Go Wild

1) Build a “Do Not Touch” Cash Buffer (So You Don’t Sell at the Worst Time)

A common reason people panic-sell is not fearit’s need. If you have to pay rent, tuition, car repairs, or a surprise medical bill, you might

be forced to sell investments when prices are down. A cash cushion (emergency fund) helps you avoid turning a temporary market drop into a

permanent personal loss.

Practical approach: keep money for short-term needs (the next 3–12 months, depending on your situation) in safer, liquid places (like a high-yield

savings account). If you’re young and your expenses are covered by family, your “emergency fund” might be smallerbut having some buffer still

reduces the chance you’ll bail out at the bottom.

2) Use Asset Allocation Like a Seatbelt, Not a Vibe

Asset allocation is simply how you split your money across major bucketsstocks, bonds, and cash (and sometimes real estate or other diversifiers).

The point is not to “win every year.” The point is to pick a mix you can stick with when markets are rude.

A classic example: if you choose 70% stocks and 30% bonds, you’re accepting that stocks may drop sharply sometimes. Bonds (and cash) are there to

reduce the portfolio’s overall whiplash and to give you “dry powder” so you’re not forced to sell stocks during a downturn.

Key idea: your best allocation is the one you can hold through volatility without panic-selling. A plan that looks great on a spreadsheet but causes

you to flee during every dip is not a plan. It’s a stress hobby.

3) Diversify Like You Mean It (Because Eggs Hate One Basket)

Diversification means spreading risk across different companies, sectors, and regionsso you’re not betting your future on one theme (or one

charismatic CEO with a podcast).

- Within stocks: own many companies (not just a few favorites).

- Across sectors: tech, healthcare, financials, industrials, consumer staples, etc.

- Across regions: consider international exposure, not only one country.

- Across asset classes: mix stocks with bonds/cash based on your goals and risk tolerance.

Broad, low-cost index funds are one common way investors diversify efficiently. The goal isn’t to eliminate risk (not possible). It’s to avoid

“single-point failure” risk.

4) Automate Investing to Outrun Your Emotions

Automation is underrated superhero stuff. Setting up recurring contributions (weekly/monthly) turns investing into a routine instead of a debate.

This is closely related to dollar-cost averaging: you invest fixed amounts over time, buying more shares when prices are lower and fewer when prices

are higherwithout trying to predict the perfect moment.

In chaotic markets, automation helps because it removes the daily “Should I wait?” spiral. You’re not timing the marketyou’re building a habit.

5) Rebalance: The Grown-Up Way to “Buy Low, Sell High”

Rebalancing means nudging your portfolio back to its target allocation when markets cause it to drift. It’s not market timing; it’s risk management.

Done right, it quietly forces you to trim what became expensive and add to what became cheapwithout needing a crystal ball.

Simple example:

- You start with 70% stocks / 30% bonds.

- A stock rally pushes you to 80% stocks / 20% bonds.

- Rebalancing means selling some stocks and buying bonds to return to 70/30 (or using new contributions to fix the drift).

You can rebalance on a schedule (e.g., once or twice a year) or with “bands” (e.g., rebalance if an asset class drifts more than 5–10 percentage

points). The best method is the one you’ll actually follow without obsessing.

6) Keep Costs Low (Because Fees Don’t Care About Your Feelings)

In volatile markets, investors often focus on what they can’t control: headlines, interest rates, and whether the market is “mad” today.

But costs are controllable. Expense ratios, trading fees, and advisory fees can quietly chip away at long-term returnsespecially if you trade a lot

during choppy markets.

Consider making “cost awareness” part of your survival plan: fewer unnecessary trades, thoughtful fund choices, and avoiding complex products you

don’t fully understand.

7) Use Tax Moves Carefully (If They Apply), and Don’t Step on the Wash-Sale Rake

For taxable accounts, some investors consider tax-loss harvesting: selling an investment at a loss to offset capital gains (and potentially a limited

amount of ordinary income, depending on tax rules), then buying a replacement investment to keep your portfolio’s strategy intact.

The big “gotcha” is the wash-sale rule. If you sell a security at a loss and buy the same or a “substantially identical” one within 30 days before or

after the sale (a 61-day window), the IRS generally disallows that loss for current tax purposes. Translation: you tried to be tax-smart and the tax

code said, “Cute.”

If you’re not confident here, keep it simpleor work with a qualified tax professional. Taxes are an area where “almost right” can still be wrong.

8) Beware of “Volatility Season” Scams and Too-Good-To-Be-True Promises

When markets get scary, scams get busy. Fraudsters love uncertainty because it makes people desperate for certainty. Be skeptical of:

- Guarantees of high returns with “no risk.”

- Pressure tactics: “Act now or miss out!”

- Unregistered sellers, vague explanations, or refusal to provide clear documentation.

- “Secret” strategies that supposedly beat the market every week.

A healthy rule: if you can’t explain how it works in plain English, you probably shouldn’t put your money into itespecially during high-volatility periods.

A Survival Checklist for the Next Time the Market Throws a Tantrum

When markets drop hard, your brain may scream, “Do something!” Here’s a calmer script:

- Zoom out: Are you investing for months, years, or decades? Your time horizon should drive your response.

- Check cash needs: If you need money soon, protect that portion from market risk.

- Review your allocation: Has it drifted? If yes, rebalance thoughtfully.

- Keep contributions steady: If you’re a long-term investor, consistency often beats cleverness.

- Reduce doom-scrolling: Markets don’t improve because you refreshed the app 47 times.

- Don’t confuse volatility with failure: Volatility is the admission price for long-term growth.

- Avoid leverage and impulse trades: Debt + volatility is a combo meal you didn’t order.

Specific Examples: What “Staying the Course” Looks Like in Real Life

Example A: The “I’m Freaking Out” Retirement Saver

Imagine someone contributing to a 401(k) every paycheck. The market drops 20%, and they’re tempted to move everything to cash.

A calmer approach:

- They keep contributions going (still buying during lower prices).

- They confirm their stock/bond mix still matches their timeline.

- They rebalance if the drop changed their allocation meaningfully.

- They avoid trying to guess the “perfect re-entry day.”

This isn’t exciting. That’s the point. In investing, excitement is often overpriced.

Example B: The “Concentrated Stock” Wake-Up Call

Another investor holds a giant position in one stock (maybe an employer stock or a favorite tech name). In chaos, that stock plunges and their entire

portfolio follows it like a toddler chasing a balloon.

A risk-reduction approach might include gradually diversifying over timespreading exposure across broader funds, sectors, and bonds/cash depending

on goals. It can reduce the chance that one company’s bad year becomes your bad decade.

Example C: The “Tax-Smart, Not Tax-Obsessed” Investor

A taxable-account investor notices a position is down. They consider harvesting losses, but they avoid wash-sale issues by not repurchasing the same

(or substantially identical) security inside the 61-day wash-sale window. They also keep records and stay within a portfolio planbecause tax moves

should support strategy, not replace it.

How to Know If Your Plan Is Too Risky (Before Chaos Exposes It)

If market volatility makes you want to abandon ship every time, your risk level may be too high for your comfort zoneor your timeline may not match

your portfolio.

Signs your plan might be misaligned:

- You can’t sleep because the market moved 2%.

- You’re relying on stock money for a near-term goal (like next year’s tuition).

- You’re heavily concentrated in one sector or one stock.

- You’re using margin/leverage to “boost returns” in a choppy market.

Adjusting risk is not admitting defeat. It’s choosing a strategy you can actually stick with.

Market Mechanics You Should Know (So You Don’t Panic Over Normal Stuff)

In extreme volatility, you may hear about trading halts or “circuit breakers.” These are rules designed to pause trading temporarily during steep

market declines, helping markets “cool off” and improving orderly price discovery. If you see a headline about a halt, it doesn’t automatically mean

the system is collapsingit often means safety mechanisms are working.

What Not to Do in Chaotic Markets (A Short Comedy in Three Acts)

- Don’t try to “win the week.” Long-term investing is not a weekly performance sport.

- Don’t make decisions while panicked. If your heart rate is doing cardio, your portfolio shouldn’t be doing gymnastics.

- Don’t confuse complexity with intelligence. Fancy strategies can be fragile strategies.

- Don’t chase hot tips. In chaos, rumors spread faster than facts.

- Don’t ignore fraud risk. Scams love fearful investors the way mosquitoes love uncovered ankles.

When to Get Help

If you’re overwhelmed, it can help to talk to someone who can bring you back to your planlike a trusted parent/guardian, a reputable financial

educator, or a licensed financial advisor. The best help doesn’t predict markets perfectly; it prevents you from making preventable mistakes.

Experiences From Chaotic Markets: 10 Lessons People Learn the Hard Way (About )

If you study real investing behavior during volatile periodswhether it was the 2008 financial crisis, the sharp pandemic-driven drop in 2020,

inflation and rate shocks in the early 2020s, or sudden sector sell-offscertain patterns show up again and again. The market changes costumes,

but investor emotions stick to the same script.

Lesson 1: The scariest days often sit right next to the best days. Many investors who “step out until things feel safer” discover that

markets can rebound quickly, sometimes before confidence returns. The emotional experience is brutal: you sell because you’re scared, then you hesitate

because you don’t want to be wrong, and the market climbs without youlike a bus that left while you were tying your shoes.

Lesson 2: People don’t panic-sell because they’re irrational; they panic-sell because they feel trapped. A common theme in volatile markets

is forced sellingsomeone loses a job, faces a big expense, or lacks a cash buffer. The market drop exposes a planning gap. That’s why experienced

investors obsess over emergency savings even when it feels boring.

Lesson 3: Concentration feels smartuntil it doesn’t. In calmer times, holding one “winner” stock feels like genius. In a chaotic market,

that same concentration can turn into a single headline ruining your month. Investors who lived through this often come out with a new respect for

broad diversification. Not because diversification is exciting, but because it reduces the chance of a portfolio being dominated by one storyline.

Lesson 4: A written plan beats a motivational quote. “Stay the course” sounds nice, but it works best when the course is clearly mapped:

target allocation, rebalancing rules, and a decision checklist for downturns. Investors who succeed through volatility often describe the same habit:

they follow the plan first and only make changes after they’ve cooled down and reviewed the facts.

Lesson 5: Automation quietly wins. People who keep investing regularly during downturns often look back and realize they bought shares at

lower prices without even trying to time it. It wasn’t bravery; it was a system. Over time, that system can matter more than any single “big call.”

Lesson 6: Chaos increases the volume of bad advice. Volatile markets attract confident predictionson social media, TV, and group chats.

Investors who survive learn to treat “sure things” with suspicion and to prioritize simple, repeatable behaviors: diversify, rebalance, keep costs low,

and focus on time horizon.

Lesson 7: The goal isn’t to feel fearlessit’s to act disciplined while feeling nervous. Even seasoned investors feel the stress.

The difference is they’ve built routines that prevent stress from controlling the buy/sell button.

Conclusion

Surviving chaotic markets isn’t about predicting the next headline. It’s about building a portfolio that matches your timeline, keeping a cash buffer

so you’re not forced to sell low, diversifying broadly, automating contributions, rebalancing calmly, controlling costs, and avoiding scams.

Volatility will still happen. The win is making sure it doesn’t hijack your long-term goals.