Table of Contents >> Show >> Hide

- The Story Behind the Headline: When a Down Payment Becomes a Family Tug-of-War

- Why “Just Give Her Half” Is Not a Simple Ask

- Affairs, Divorce, and Money: What Actually Matters (And What Usually Doesn’t)

- The Emotional Logic Behind the Pressure: Why Families Target the “Responsible” One

- What the Pregnant Woman Is Really Protecting

- Practical Steps: How to Respond Without Burning Down the Family Group Chat

- Specific Examples: What Different “Help” Paths Can Look Like

- 500-Word Experience Section: What People Learn the Hard Way in Deposit Disputes

- Conclusion: A Deposit Is Not a Family Emergency Fund

There are family conflicts, and then there are family conflictsthe kind that make you stare at your banking app like it just personally betrayed you.

In one widely shared online story, a pregnant woman and her partner had spent years building a house deposit (the sacred pile of money that turns “we’re browsing listings”

into “we’re scheduling inspections”). Then her sister blew up her own marriage, left her kids and husband for an affair partner, and quickly found herself in a housing crisis.

The twist? Some relatives decided the solution was simple: the pregnant woman should hand over half of her house deposit so the sister could secure a place to live.

If your stomach just did a little somersault, congratulationsyou’re emotionally fluent in boundaries.

This article breaks down why this kind of request is so explosive, what’s actually at stake financially and legally, and how to respond without turning Thanksgiving into

“The Great Gravy Reckoning.” We’ll keep it real, keep it human, and yeskeep it a little funny, because sometimes you have to laugh so you don’t scream into a pillow.

The Story Behind the Headline: When a Down Payment Becomes a Family Tug-of-War

The online post (shared and discussed across major forums and commentary sites) follows a familiar arc: one sibling makes a series of high-drama choices, the consequences arrive,

and then the family forms a committee to decide who should pay for them. In this case, the sister’s choices led to instabilityrelationship fallout, strained co-parenting, and

housing insecurity. Instead of focusing on realistic options (temporary housing, budgeting, or support programs), the family locked onto the pregnant woman’s house deposit as

the “available resource.”

That’s not just an emotional gut-punch. It’s also a financial landmine. A house deposit isn’t “extra money.”

For most buyers, it’s the difference between qualifying and not qualifying, between manageable monthly payments and “guess I live in my car now.”

And when someone is pregnant, that deposit can feel even more urgentbecause stability stops being a vibe and starts being a necessity.

Why a House Deposit Feels So Personal

A deposit is often years of discipline: skipping trips, living with a too-small couch, saying “no thanks” to brunch that costs the same as a small appliance.

It’s also future planning in cash formsafety, a nursery, a predictable monthly payment, and a sense that you’re building something solid.

So when family says, “Give half away,” what they’re really saying is, “Trade your stability for my emergency.”

That’s why people don’t just feel annoyed; they feel violated.

Why “Just Give Her Half” Is Not a Simple Ask

Let’s zoom out from the drama and look at the money mechanics. There are two deposits people often confuse:

(1) a down payment (your contribution toward the purchase price) and (2) earnest money (a “good faith” deposit held in escrow once an offer is accepted).

Either way, it’s not cash you can casually reassign like you’re Venmo-ing for pizza.

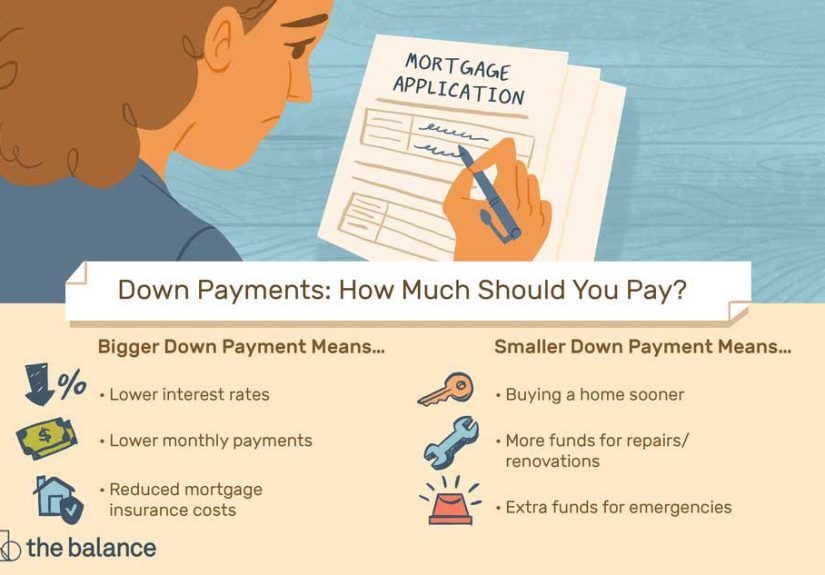

Down Payment vs Earnest Money: The Two “Deposits” That Matter

- Down payment (house deposit): Money you bring to closing to reduce the loan amount and improve loan terms. Smaller down payments can mean higher monthly payments,

private mortgage insurance (PMI), or failing underwriting thresholds altogether. - Earnest money: Money you put down after the seller accepts your offer. It’s typically held by a neutral third party and may become nonrefundable if contingencies are waived

or deadlines pass. In many contracts, disputes about who gets it can delay or complicate refunds.

So when someone says “half your deposit,” they might be talking about the down payment you still need to closeor money that is already tied up in escrow and governed by a contract.

In both cases, the idea that it’s just “sitting there” is a misunderstanding of how home buying works.

The Gift-or-Loan Problem: Family Money Gets Messy Fast

Even if the pregnant woman wanted to help, handing over tens of thousands of dollars creates a second crisis: Is it a gift or a loan?

Mortgage underwriting often requires documentation for large transfers. If the money is a gift, lenders commonly expect a signed gift letter stating it does not need to be repaid.

If it’s a loan, that new monthly obligation can change the borrower’s debt-to-income ratio and affect approval.

Translation: “I’m helping my sister” can accidentally turn into “I just torpedoed my mortgage.”

And if the family expects repayment “someday,” but nothing is in writing, you’ve created the classic heartbreak:

one person thinks it was a loan, the other person thinks it was a gift, and everyone thinks you ruined Christmas.

Affairs, Divorce, and Money: What Actually Matters (And What Usually Doesn’t)

The headline includes the affair because it explains the emotional temperature. But legally, infidelity often matters less than people assumeespecially in no-fault divorce states.

Courts generally focus on finances, fairness, and children’s best interests, not moral scoring.

However, there’s a big exception that shows up in many states under different names: wasting marital assets (often called “dissipation” or “marital waste”).

When Cheating Impacts the Money: Dissipation and “Marital Waste”

If a spouse spends significant marital funds on an affairthink gifts, trips, rent, secret credit card paymentsthat spending may be argued as misuse of marital assets.

In some cases, courts can account for that when dividing property, effectively treating the spender as having already taken an “advance” on their share.

This doesn’t mean “cheater loses everything,” but it can matter if the spending is substantial and provable.

Why does this matter to the pregnant woman’s deposit fight? Because families often mix up two separate issues:

(1) the sister’s divorce finances and housing needs, and (2) the pregnant woman’s separate savings and home plan.

The sister’s divorce should be handled through legal channels, budgeting, and support systemsnot by raiding a sibling’s deposit fund as an emergency ATM.

The Emotional Logic Behind the Pressure: Why Families Target the “Responsible” One

Here’s the uncomfortable truth: families often pressure the most stable person because they’re the easiest to pressure.

The responsible sibling is predictable. They save. They plan. They feel guilty. They respond to group texts.

Meanwhile, the chaotic sibling is… chaotic. Arguing with them feels like trying to nail Jell-O to a wall.

So the family subconsciously chooses the path of least resistance: squeeze the stable person until money appears.

Guilt Is a Tool (Even If Nobody Admits They’re Using It)

When relatives say, “But she’s your sister,” they’re not offering a financial planthey’re applying emotional leverage.

You’ll hear words like selfish, cold, heartless, or the all-time classic: family helps family.

Notice how rarely anyone says, “Here’s a budget, a timeline, and a written agreement.” Guilt is cheaper than planning.

Boundary experts often point out that saying “no” can feel wrong if you were raised to prioritize others’ comfort over your own needs.

That’s why people can feel anxious even when their decision is financially rational.

The goal isn’t to become a robot. It’s to learn to be compassionate without being financially volunteered.

What the Pregnant Woman Is Really Protecting

From the outside, people may frame this as “money vs sister.” But it’s not that simple.

She’s protecting:

- Her housing security (and her baby’s stability).

- Her relationship with her partner, who also saved for the deposit.

- Her financial futurebecause losing the deposit can delay buying by years.

- Her autonomythe right to decide what her savings are for.

And yes, she may also be protecting the sister from a different kind of harm: enabling.

If every crisis gets bailed out, the crisis becomes the strategy. Help that prevents growth is not always help.

Practical Steps: How to Respond Without Burning Down the Family Group Chat

1) Get Crystal Clear on the Numbers

Before responding, calculate what “half” really means. Would it drop you below a target down payment percentage?

Would it increase PMI? Would it change your mortgage rate, monthly payment, or ability to qualify?

When you know the concrete impact, it’s easier to stand firm without getting pulled into emotional arguments.

2) Use a Calm, Repeatable Script

You don’t owe a 40-slide presentation. A short script is powerful:

“We can’t give away our house deposit. That money is committed to our home purchase and our baby’s stability.”

Repeat as needed. Calm is your superpower.

3) Don’t Negotiate Against Yourself

If you say “no,” pause before offering alternatives you can’t sustain.

People sometimes soften a boundary with, “But maybe later,” which becomes a permanent opening for pressure.

If later isn’t realistic, don’t promise it. You can be kind without being vague.

4) If You Give Anything, Put It in Writing

If you choose to help financially (even a small amount), protect everyone with clarity:

is it a gift, a one-time emergency payment, or a loan with terms? Written agreements prevent “selective memory”

from becoming a second disaster. It also discourages repeat requests based on assumptions.

5) Separate “Housing Help” From “House Deposit”

If the sister truly needs support, focus on options that don’t sabotage your home purchase:

helping research assistance programs, connecting her with legal aid, contributing to a temporary expense (like a week in a motel),

or paying for a consultation with a family law attorney or housing counselor.

Support isn’t only cashand it definitely doesn’t have to be your down payment.

Specific Examples: What Different “Help” Paths Can Look Like

Example A: Temporary Support With Firm Limits

You offer a one-time amount that won’t affect your home purchasesay, help with first month’s rent or a security deposit

and you state clearly it’s not repeatable. You also insist the sister create a plan (income, budget, timeline).

This is assistance without surrendering your long-term goal.

Example B: Non-Financial Help That Still Matters

You help her apply for services, look for jobs, locate short-term housing, or set up childcare resources.

This is especially useful if the sister’s crisis is partly logistical.

It’s not as flashy as writing a huge checkbut it can be more effective.

Example C: The “Written Agreement or No Money” Boundary

If you do lend money, you document it. Amount, repayment schedule, what happens if payments stop.

This tends to either (1) improve accountability or (2) magically reduce the urgency of the request.

Either outcome is informational.

500-Word Experience Section: What People Learn the Hard Way in Deposit Disputes

If you’ve never had a family member eye your savings like it’s a community swimming poolcongratulations, you’re living in a rare ecosystem.

For everyone else, stories like this hit a nerve because they’re recognizable. Not always with a house deposit, but with the same pattern:

someone makes a risky choice, consequences land, and the “responsible one” is asked to absorb the impact.

Here are common experiences people share when money, siblings, and housing collidealong with the lessons that tend to stick.

Experience #1: “I helped once, and now it’s the expectation.”

Many people describe offering a one-time bailoutrent, a car repair, a depositthinking it would bridge a short gap.

But the family narrative quietly shifts from “You helped” to “You can help.” Then “You should help.” Then “You must help.”

The lesson: if you give, define it. Put a cap on it. Say it out loud: “This is one-time only.”

Boundaries are kinder when they’re clear, because they prevent resentment from building in silence.

Experience #2: “They didn’t want support; they wanted control of the money.”

People often offer alternativesjob leads, budgeting help, temporary housing optionsand get rejected.

That’s a signal. If every non-cash solution is dismissed, the problem may not be the crisis itself; it may be the desire to access your funds.

The lesson: don’t confuse rejection of your help with proof you need to give more. Sometimes it’s proof your boundary is necessary.

Experience #3: “I tried to be fair, and it still wasn’t enough.”

In families with long-standing favoritism or “the squeaky wheel gets the grease,” the responsible sibling can feel trapped in a fairness game they can’t win.

If you give a little, you’re asked for more. If you say no, you’re labeled selfish.

The lesson: fairness isn’t measured by how uncomfortable you make yourself. It’s measured by whether everyone is being asked to carry an appropriate share of responsibility.

A grown adult’s housing plan cannot permanently depend on another sibling’s sacrifices.

Experience #4: “Pregnancy (or any big life change) exposes weak boundaries fast.”

People who are starting families, changing jobs, or buying homes often notice that relatives become more opinionated about their money.

It’s as if the family sees forward progress and thinks, “They can spare it.”

The lesson: stability can make you a target. Protecting your deposit isn’t greedit’s prioritizing the life you’re actively building.

If your budget is tight enough that losing half the deposit delays your home purchase, you don’t “have extra.” You have a plan.

Experience #5: “The relationship improved when I stopped paying for peace.”

This one surprises people. When you stop funding the chaos, the emotional temperature may spike at firstanger, guilt trips, silence.

But over time, some families reset: either the person adapts and becomes more self-sufficient, or the dynamic changes so you’re no longer the automatic solution.

The lesson: you can’t buy lasting harmony. You can only rent it, and the renewal fee goes up every time you pay.

If you’re in a similar situation, the goal isn’t to punish anyone. It’s to make choices that protect your future and your mental health.

Compassion is a value. So is stability. You’re allowed to hold both.

Conclusion: A Deposit Is Not a Family Emergency Fund

This headline is dramatic, but the core lesson is surprisingly practical: your house deposit has a job.

Its job is to help you buy a home, qualify for a mortgage, and build stabilityespecially when a baby is on the way.

Your sister’s crisis may be real. Your empathy may be real. But that does not automatically turn your savings into a shared asset.

If the sister needs help, there are pathslegal guidance, housing resources, budgeting, temporary support that doesn’t derail your future.

What isn’t sustainable is the idea that the most responsible person should finance everyone else’s consequences.

You can love your family and still say, “No. Not this money. Not this plan.”

And if anyone calls you selfish for protecting your baby’s home? Let them.

Selfish is taking half a pregnant woman’s deposit. You’re just being housed.