Table of Contents >> Show >> Hide

- Why time horizon is the boss of your retirement plan

- The 4% rule: what it is, what it isn’t, and why it won’t stop calling you

- A Wealth of Common Sense math: the “spending your principal” reality check

- Meet the real villains: inflation and sequence-of-returns risk

- So what withdrawal rate should you use?

- Flexibility beats heroics: dynamic strategies that behave more like real life

- Asset allocation: you can’t outlast inflation on “safe” alone

- Social Security: the withdrawal-rate lever hiding in plain sight

- Taxes, RMDs, and why your withdrawal rate is not just “spending”

- A practical playbook: build a withdrawal plan that can survive reality

- Common mistakes (aka the ways retirement plans get spicy)

- Experiences from real retirement life: what the spreadsheets don’t warn you about (extra section)

- 1) The “first five years are expensive” surprise

- 2) The market downturn that shows up right on schedule (your schedule)

- 3) The “we’re spending too little” realization

- 4) The tax ambush: “Why is my withdrawal so much bigger than my spending?”

- 5) The family factor: adult kids, grandkids, and the “we didn’t model this” category

- Conclusion: common sense retirement spending is flexible, not fragile

Retirement planning is basically a game of “How long does this pile of money need to behave?” If your answer is

“about 20 years,” you can play one way. If your answer is “uh… possibly 35 to 40 years, and I’d like to help my kids

and spoil my grandkids,” you’re playing an entirely different sportsame ball, different rules, much more sweating.

The tricky part is that the biggest driver of your withdrawal rate isn’t your personality type (though “I panic-sell in a

mild breeze” matters). It’s your time horizon: the number of years your portfolio needs to fund your life,

plus a little extra for life’s favorite surprise side questsroofs, medical bills, family emergencies, and that one

“once-in-a-lifetime” trip that somehow becomes annual.

This article breaks down the common-sense logic behind time horizons and withdrawal rates, why the famous “4% rule” is

helpful but not holy, and how real retirees can build a spending plan that’s sturdy enough to handle inflation, market

drama, and the fact that you’re a human who occasionally wants to buy something nice.

Why time horizon is the boss of your retirement plan

Picture two retirees with identical portfolios: $1,000,000 invested in a diversified mix of stocks and bonds.

Retiree A is 70, has strong pension income, and mainly needs the portfolio as a backup. Retiree B is 62, no pension,

and the portfolio is the paycheck. Same number on paper. Different reality.

Time horizon shapes almost everything:

- How much you can withdraw without raising the odds of running out.

- How much inflation matters (spoiler: it always matters, but longer horizons get hit harder).

- How much stock exposure you need to outpace rising costs over decades.

- How much flexibility you should build in for down markets and big spending years.

A “safe” withdrawal rate isn’t a single number. It’s a range that depends on your timeline, your spending mix

(must-have vs. nice-to-have), and how willing you are to adjust when markets misbehave.

The 4% rule: what it is, what it isn’t, and why it won’t stop calling you

The 4% rule became famous because it’s simple: withdraw 4% of your portfolio in the first year of retirement, then

raise that dollar amount each year with inflation. If you retire with $1,000,000, that’s $40,000 in year one.

If inflation runs 2%, you take $40,800 in year two, and so on.

The part people love: a clean starting point

Humans like rules of thumb. They reduce anxiety and spreadsheet time. And as a planning toolespecially for early

retirement modeling and savings goalsthe 4% rule has real value. It forces you to connect lifestyle spending to the

size of the nest egg, which is the correct direction of travel.

The part people forget: it’s a “30-year-ish” tool, not a lifetime guarantee

The classic framing assumes a roughly 30-year retirement horizon. If your horizon is longer (early retirement, family

longevity, or simply “I’m not trying to speedrun life”), the same starting withdrawal rate carries more risk.

If your horizon is shorter, a strict 4% may be overly cautiousmeaning you might be accidentally living on

rice and beans while your portfolio grows old and untouched out of spite.

It’s also rigid. The inflation adjustment doesn’t care if markets are down 25%. It doesn’t care if you’re spending less

naturally in later years. It doesn’t care if you have a huge year-one expense (new car, home remodel, dream trip).

It just shows up, clipboard in hand, and says: “Your raise is due.”

A Wealth of Common Sense math: the “spending your principal” reality check

One of the most clarifying insights from the “time horizons & withdrawal rates” discussion is that many retirees

mentally treat their portfolio like a protected treasure chest. But a retirement portfolio is not a museum exhibit.

It’s a tool. And tools get used.

Here’s the simplest way to see why time horizon matters: in real (inflation-adjusted) terms, a constant-dollar strategy

behaves like withdrawing the same percentage of your starting portfolio each year.

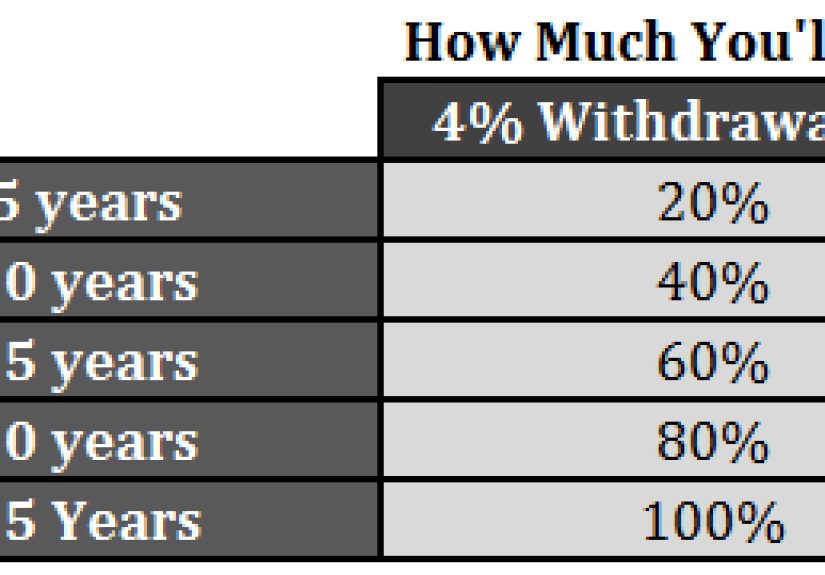

- 4% per year means you withdraw roughly 4% of the original principal annually (in real terms).

- Over 10 years, that’s about 40% of the starting principal.

- Over 20 years, it’s about 80%.

- Over 25 years, you’ve withdrawn about 100% of the starting principal.

That doesn’t mean you’re “out of money” after 25 yearsbecause investments can grow. But it highlights the core point:

if your portfolio only keeps pace with inflation (meaning no real growth), a 4% inflation-adjusted

withdrawal schedule drains the pile in about 25 years. At 5%, it’s about 20 years. At 3%,

it’s closer to 33 years. The withdrawal rate is inseparable from the timeline.

Meet the real villains: inflation and sequence-of-returns risk

Inflation: the quiet pickpocket

Inflation doesn’t make headlines until it does, but it’s always working. If your retirement might last 30–40 years,

your spending plan has to keep up. That’s why most strategies either (a) include inflation adjustments, or

(b) build in some market-linked flexibility that still aims to preserve purchasing power over time.

Sequence-of-returns risk: timing matters more than you’d like

Two retirees can earn the same average return over 30 years and still have wildly different outcomes if one gets a

bad market early. Early losses plus withdrawals can create a “double hit”: you’re selling more shares when prices are

low, so fewer shares remain to rebound later.

This is why a plan that looks perfect in an average-return spreadsheet can still fail in real life. A simple illustration:

when early retirement years include market declines, dialing back withdrawals can dramatically improve recovery time.

The practical lesson isn’t “be terrified,” it’s “build flexibility so you don’t have to sell aggressively into downturns.”

So what withdrawal rate should you use?

The honest answer: start with your life, not a headline number. Your starting withdrawal rate is a

reflection of the gap between your spending and your other income sources (Social Security, pensions, part-time work,

rental income), plus your tolerance for adjusting along the way.

Here’s a practical framework that blends research, common retirement planning guidance, and reality:

1) Estimate your “must-have” spending vs. “nice-to-have” spending

Separate essentials (housing, utilities, food, insurance, health care) from flexible goals (travel, gifting, hobbies,

upgrades, “because I deserve it” purchases). The goal is to avoid forcing your portfolio to fund all spending the same way.

2) Match essentials to reliable income when possible

Many planning approaches emphasize covering core expenses with stable income sourcesSocial Security, pensions,

and (for some households) annuitiesthen using portfolio withdrawals for the rest. This reduces stress and increases

your ability to be flexible during market downturns.

3) Choose a starting rate based on horizon and flexibility

As a broad rule of thumb for a traditional 30-year retirement, many mainstream retirement education resources still

discuss a starting range around 4%–5% for an inflation-adjusted approachespecially when paired with a

diversified portfolio and some willingness to adapt. But forward-looking research in recent years has often suggested

more conservative starting points for new retirees (think high-3% range), depending on expected returns and inflation.

A simple way to think about it:

- Shorter horizon (15–20 years): you may be able to start higher, especially with other income.

- Classic horizon (25–30 years): the “4% rule” neighborhood is a reasonable planning baseline.

- Long horizon (35–40+ years): consider starting lower or using flexible/dynamic methods.

- Very long horizon (early retirement / 50+ years): flexibility matters even more; rigid rules get shaky.

Flexibility beats heroics: dynamic strategies that behave more like real life

Most retirees don’t spend the same inflation-adjusted amount every year forever. Life has seasons. Spending can be

higher early (travel, activities), then lower later, then higher again if health costs rise. Good strategies acknowledge

this instead of pretending you’re a robot with a fixed annual “spending protocol.”

Guardrails: spend more when it’s safe, cut back when it’s not

“Guardrails” strategies aim to boost sustainability by setting rules for when to tighten the belt and when to loosen it.

One well-known research line (often referenced in retirement income planning circles) uses decision rulessuch as

freezing inflation increases after poor returns, or applying spending cuts if withdrawals drift too high relative to the

portfolio. The goal is not perfection; it’s to avoid stubbornly increasing spending in the worst possible years.

The key benefit is psychological: instead of guessing, you have a pre-committed plan. That matters, because the market

loves to show up when you’re most emotionally vulnerable and whisper, “Now would be a great time to panic.”

Dynamic spending with a floor and a ceiling

Another practical approach combines two ideas: keep spending somewhat stable (so you can live your life), but still let

spending react to markets (so your money lasts). A common version is:

- Start with a reasonable dollar amount (like the 4% rule style baseline).

- Each year, adjust based on portfolio performance.

- But don’t exceed a “ceiling” or fall below a “floor” you pre-set.

This is common sense in action: you’re not pretending downturns don’t exist, but you’re also not accepting a lifestyle

freefall when markets have a rough year.

Bucket strategies: give spending money a job (and a time horizon)

Bucket strategies split money into time-based pools:

- Bucket 1 (now): cash for near-term spending.

- Bucket 2 (soon): conservative bonds/fixed income for mid-term needs.

- Bucket 3 (later): equities for long-term growth and inflation defense.

Done well, buckets can help you avoid selling stocks in a bear market to fund next year’s groceriesbecause your

“groceries” bucket is already funded. This doesn’t eliminate risk, but it can reduce the behavioral risk of making

terrible decisions at terrible times.

Asset allocation: you can’t outlast inflation on “safe” alone

If retirement might last 30–40 years, inflation is a long opponent. That’s why many retirement frameworks still include

meaningful stock exposure: not because you love volatility, but because you need long-term growth to keep purchasing

power from eroding.

There’s also a counterintuitive idea supported by retirement research: some portfolios may benefit from increasing

equity exposure later in retirement (a “rising equity glidepath”), especially as a response to poor early returns.

The logic is basically: if markets are bad early, you don’t want to lock in low-growth forever. You want the engine

that can help you recovermanaged carefully, not recklessly.

This is not a one-size-fits-all solution. It’s a reminder that retirement isn’t just “de-risk until you’re 100% cash and

vibes.” It’s risk management over decades, and the best risk management is often more nuanced than “sell all stocks.”

Social Security: the withdrawal-rate lever hiding in plain sight

Social Security is one of the most powerful “withdrawal rate” tools because it can reduce the amount your portfolio

needs to provide. Delaying benefits beyond full retirement age increases monthly payments by a set percentage per year

(for many retirees, 8% per year), and the increase stops at age 70.

Why this matters: if delaying Social Security raises guaranteed income later, you may be able to withdraw a little more

from the portfolio in early years (to bridge the gap), and then withdraw less later. In other words, you can sometimes

trade early portfolio spending for higher lifelong incomereducing longevity risk.

It’s not always optimal to delay (health, spouse benefits, cash flow needs), but it’s worth modeling. Think of it as a

“raise” you can buy by waitingone that can lower long-term portfolio pressure.

Taxes, RMDs, and why your withdrawal rate is not just “spending”

Many people plan a withdrawal rate as if every dollar withdrawn becomes a dollar spent. In reality, taxes and account

rules can turn withdrawals into a different number than the one you budgeted.

Required minimum distributions can force higher withdrawals later

Traditional IRAs and many workplace retirement plans have required minimum distributions (RMDs). Under current rules,

the first RMD is tied to reaching age 73, and the first-year timing can create a “two distributions in one year” problem

if you delay the first withdrawal until April 1 of the following year. That can spike taxable income and ripple into

Medicare premiums and taxation of Social Security benefits.

Withdrawal order and Roth strategy can change outcomes

Tax planning can extend portfolio longevity without changing your lifestyle. For example, some strategies use Roth

conversions in lower-income years early in retirement to reduce later tax burdensespecially once Social Security and

RMDs begin. The goal isn’t to play tax games; it’s to avoid paying higher lifetime taxes simply because timing was ignored.

Your “safe withdrawal rate” should really be thought of as a net spending rate:

what you can spend after taxes, healthcare premiums, and other friction costsnot just what leaves the account.

A practical playbook: build a withdrawal plan that can survive reality

If you want a retirement plan that feels like a grown-up version of common sense (instead of a fragile math trick),

try this sequence:

- Define your horizon: plan for 30 years unless you have a strong reason not to; consider 35–40 if retiring early or family longevity is high.

- Budget essentials vs. flex: know what must be funded no matter what.

- Map guaranteed income: Social Security, pensions, and other stable sources.

- Pick a starting rate: use a conservative baseline if you want fewer “oh no” moments; start higher only if you can cut back when needed.

- Choose a spending method: guardrails, floor/ceiling dynamic spending, or a bucket plananything that lets you adapt.

- Build a cash buffer: enough to avoid forced selling in a downturn (your “sleep at night” fund).

- Review annually: not daily (you deserve peace), but at least yearly (you deserve competence).

None of this requires perfect forecasting. It requires structure, flexibility, and the humility to admit that markets

don’t care about your retirement date.

Common mistakes (aka the ways retirement plans get spicy)

- Using one withdrawal rate for all horizons (20 years and 40 years are not the same movie).

- Ignoring taxes until April makes you cry.

- Assuming spending is flat when your life is clearly not flat.

- Overreacting to markets (your portfolio is a long-term tool, not a mood ring).

- Not planning for big expenses like healthcare, housing transitions, or family support.

Experiences from real retirement life: what the spreadsheets don’t warn you about (extra section)

Retirement research is full of charts and probabilities, but the lived experience usually comes down to a handful of

recurring moments. Here are common scenarios retirees describeeach one directly tied to time horizons and withdrawal

rates, and each one worth planning for ahead of time.

1) The “first five years are expensive” surprise

Many retirees imagine spending will drop the moment work ends. Sometimes it does (commuting, work wardrobe, lunches).

But often the first phase of retirement is a “go-go” season: travel, hobbies, visits with family, home projects, and

delayed fun. The result is a front-loaded spending patternhigher withdrawals early, lower later.

This is where rigid inflation-adjusted rules can be awkward. A better fit is a plan that intentionally allows higher

spending early with guardrails, so you can enjoy the healthy years without accidentally setting a permanent

spending level your portfolio can’t support through a 35-year horizon.

2) The market downturn that shows up right on schedule (your schedule)

Retirees often say some version of: “Of course the market dropped right after I retired.” It’s not personal; it’s just

the math of sequence-of-returns risk. The emotional experience is real, though: watching balances fall while you’re

withdrawing can feel like trying to bail out a canoe with a teaspoon.

Retirees who have a cash buffer or a bucket strategy frequently describe the same benefit: calm. Even if the portfolio

is down, they know next year’s spending doesn’t require selling stocks at a discount. That calm leads to better

decisions, which is the underrated superpower of a sustainable withdrawal plan.

3) The “we’re spending too little” realization

Another common experience is underspending. Some retirees remain so cautious that they don’t use the resources they

worked decades to build. This can happen when people treat the 4% rule as a ceiling rather than a starting point, or

when they fear any spending increase will trigger disaster.

A time-horizon lens can help here. If you’re 75, have stable Social Security income, and your spending is naturally

declining, a rigid 30-year, near-100%-success withdrawal framework may be unnecessarily conservative. For many

retirees, a reasonable probability of success plus flexibility can unlock more meaningful life spending today.

4) The tax ambush: “Why is my withdrawal so much bigger than my spending?”

People are often surprised by how taxes reshape retirement cash flow. RMDs can force larger distributions than you

“need,” and Social Security taxation can create frustrating marginal-rate spikes. Retirees who didn’t plan for this

sometimes end up withdrawing more than intended, not to spend, but to satisfy rules and pay the IRS.

Those who did planusing thoughtful withdrawal sequencing, Roth conversions in lower-tax years, and charitable giving

strategies where appropriateoften report a smoother ride. The experience isn’t “I beat the system.” It’s “I reduced

surprises,” which is the adult version of winning.

5) The family factor: adult kids, grandkids, and the “we didn’t model this” category

Retirement plans often assume spending is mostly about the retiree household. Real life includes helping family, being

generous, and sometimes stepping in financially during someone else’s rough patch. That generosity is meaningful, but

it changes your time horizon mathespecially if you want to preserve an inheritance.

Retirees who feel good about these choices often share one habit: they separate “lifestyle spending” from “family/legacy

spending,” sometimes even using separate accounts or mental buckets. It helps them give joyfully without accidentally

drifting into a withdrawal rate that threatens long-term sustainability.

Conclusion: common sense retirement spending is flexible, not fragile

Withdrawal rates aren’t about finding the perfect number. They’re about designing a plan that matches your time horizon

and behaves well in both good markets and bad ones. A rigid rule can be a useful starting point, but a

flexible spending framework is what keeps retirement from becoming a decade-long stress test.

If you remember one thing, make it this: your retirement horizon is the real withdrawal rate engine.

The longer the horizon, the more you need inflation protection, a strategy for sequence risk, and a plan that can bend

without breaking. Because retirement isn’t a math contest. It’s your life.

Educational information only; consider working with a qualified financial and tax professional for personalized guidance.