Table of Contents >> Show >> Hide

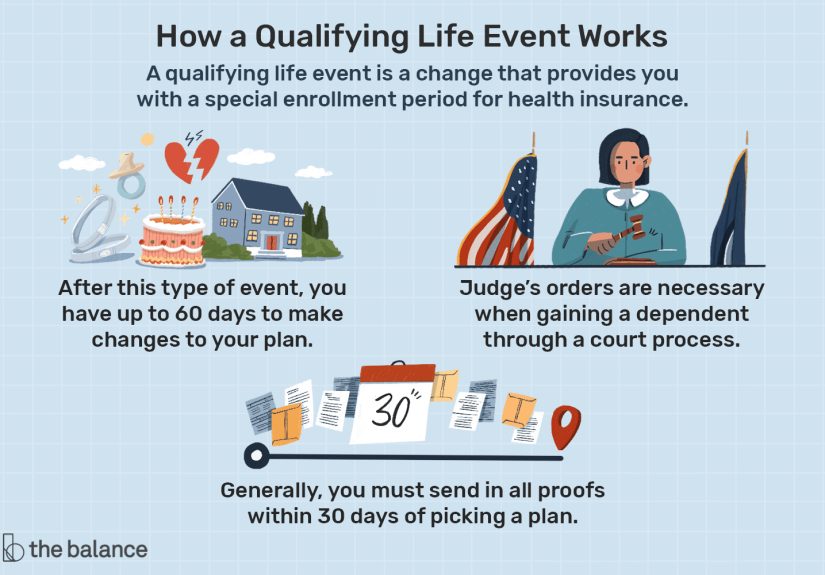

- Qualifying Life Event, in Plain English

- The Main Types of Qualifying Life Events

- How Special Enrollment Periods Work

- Qualifying Life Events Beyond Medical Insurance

- Documentation: Proving Your Qualifying Life Event

- Practical Tips to Navigate a Qualifying Life Event

- Real-World Experiences with Qualifying Life Events

- Bottom Line

If you’ve ever tried to change your health insurance outside of open enrollment, you’ve probably heard the mysterious phrase

“qualifying life event” (QLE). It sounds like something out of a video game: “You’ve unlocked a new life eventpress

X to change your coverage.” In reality, it’s a very real concept in U.S. benefits and health insurance law, and it can make the

difference between staying covered and being stuck with no insurance at all.

In this guide, we’ll break down what a qualifying life event is, which situations usually count, how the timing rules work, and

what you need to do when life changes and your insurance needs to change with it. We’ll also walk through real-world experiences

and practical tips to help you avoid common mistakes.

Qualifying Life Event, in Plain English

What is a qualifying life event?

A qualifying life event is a significant change in your lifelike getting married, having a baby, losing your job, or

movingthat lets you sign up for or change health insurance outside of the normal open enrollment period.

Normally, health insurance planswhether through the ACA Marketplace, your employer, or a private insureronly

allow you to enroll or make changes once a year during open enrollment. QLEs are the “exception rules” that

open a Special Enrollment Period (SEP) when something big in your life affects your coverage.

Why do qualifying life events matter?

QLEs matter because health care is expensive, and going without coverage (even for a short stretch) can be very risky. A qualifying

life event:

- Lets you enroll in a new plan if you don’t currently have coverage.

- Allows you to change plans (for example, from a bronze to a silver Marketplace plan or from employee-only to family coverage).

- Can help you avoid gaps in coverage when your old plan ends.

Think of a QLE as the legal “excuse” that lets you adjust your insurance mid-year without having to wait for the next open enrollment.

The Main Types of Qualifying Life Events

While the exact rules vary slightly between Marketplace plans, employer plans, and other types of insurance, most sources group

qualifying life events into four main buckets:

1. Loss of health coverage

One of the most common QLEs is losing your existing health coverage. This usually includes:

- Losing job-based coverage because you leave your job, are laid off, or your hours drop below the eligibility threshold.

- Losing COBRA coverage when it ends or when you can no longer afford it.

- Timing out of a parent’s plan, usually at age 26, under federal rules.

- Losing eligibility for Medicaid or the Children’s Health Insurance Program (CHIP).

- Having your individual health plan terminated due to insurer actions (for example, the company exits your region’s market).

Important nuance: for Marketplace coverage, the loss usually must be involuntary. Canceling your own plan or not paying

premiums typically does not count as a qualifying life event.

2. Household changes

These are the major life moments everybody posts about on social mediaexcept here they come with paperwork:

- Marriage – You can usually add your spouse and possibly stepchildren to your plan or join theirs.

- Divorce or legal separation – You may lose access to a spouse’s plan and need your own coverage, or you might remove an ex-spouse from your plan.

- Birth, adoption, or placement of a child – You can enroll a new dependent and may also be allowed to change your plan level.

- Death of a covered family member – This can affect eligibility and premium-sharing for the rest of the household.

These events don’t just change your Facebook relationship statusthey change who needs coverage, who pays for it, and how much you may owe.

3. Changes in residence

Health insurance is surprisingly “geographical.” Moving can be a qualifying life event if it changes which plans are available to you, such as:

- Moving to a new state or sometimes a new county or ZIP code.

- Moving into or out of a service area for a specific health plan.

- Students moving for college, or seasonal workers changing locations.

If your move affects your plan’s provider network or makes your old plan unavailable, that typically opens a Special Enrollment Period.

4. Other qualifying life events

Some QLEs don’t fit neatly into the categories above but still affect your eligibility:

- Gaining or losing eligibility for government programs like Medicare, Medicaid, or CHIP.

- Changes in immigration or citizenship status that affect your ability to enroll.

- Leaving incarceration, which can open access to Marketplace plans.

- Other plan-specific events defined in your employer’s or insurer’s rules (for example, a spouse starting or leaving a job with benefits).

Employers and insurers may also use related concepts like “change in status” under IRS Section 125 cafeteria plan rules to define

when you can change pre-tax elections for premiums and flexible spending accounts.

How Special Enrollment Periods Work

Deadlines: how long do you have to act?

Most qualifying life events give you a limited windowknown as a Special Enrollment Period (SEP)to change your coverage:

- ACA Marketplace plans: typically 60 days before or after the qualifying life event.

- Employer-sponsored plans: often 30 days from the date of the event (for example, 30 days after your wedding or your child’s birth).

Miss the deadline, and you may have to wait until the next open enrollment periodsometimes months away. That’s why HR and benefits

folks always nag you to “submit your paperwork right away.”

Effective dates: when does new coverage start?

The effective date of your new coverage depends on the specific event and when you submit your application:

- For many Marketplace plans, if you enroll by the 15th of a month, coverage often starts on the 1st of the following month.

- For birth, adoption, or placement, coverage can often be backdated to the date of the event to avoid gaps for the child.

- Employer plans may have similar “first of the next month” rules, but details vary by plan.

Always check the exact rules for your planthe timing of when you submit forms can matter just as much as the event itself.

What doesn’t count as a qualifying life event?

Some changes feel big in your personal life but do not usually qualify you for a Special Enrollment Period. Examples include:

- Deciding you simply want a cheaper plan mid-year.

- Voluntarily canceling your current coverage (as opposed to losing it involuntarily).

- Minor changes in income (unless they cause a change in eligibility for subsidies or programs like Medicaid).

- Routine changes in health status, like being diagnosed with a conditionunfortunately, needing more care doesn’t automatically open enrollment.

That’s one of the quirks of the system: you often need the life event before the health event to get in the door.

Qualifying Life Events Beyond Medical Insurance

The term “qualifying life event” shows up most often in health insurance, but similar rules apply to other benefits:

- Dental and vision plans: Often follow the same QLE rules as your medical plan.

- Life insurance: Marriage, divorce, or the birth of a child may let you increase or decrease coverage or update beneficiaries.

- Flexible Spending Accounts (FSAs) and dependent care FSAs: Section 125 “change in status” rules allow mid-year election changes when your family or work situation changes.

Employers may be more or less generous in how they implement these rules. IRS guidelines set the outer limits, but each plan chooses

which events it will recognize and how flexible it will be.

Documentation: Proving Your Qualifying Life Event

In a perfect world, you’d just say “I got married” and your insurer would nod and update your account. In the real world, you’ll

usually need to prove your qualifying life event with documents like:

- Marriage certificate, divorce decree, or legal separation order.

- Birth certificate, adoption papers, or placement documents.

- Letter from your employer or insurer confirming loss of coverage and the date it ends.

- Lease agreement, utility bill, or other proof of your new address for moves.

For Marketplace plans, you may have to upload documents online before your new coverage fully kicks in. For employer plans,

HR will usually tell you exactly what they need and where to send it.

Practical Tips to Navigate a Qualifying Life Event

1. Mark the dateit matters

The clock on your Special Enrollment Period usually starts on the date of the eventwedding day, move-in date, last day of prior

coverage, birthday, etc. Put that date somewhere you won’t forget; your enrollment deadline is anchored to it.

2. Talk to HR or a navigator early

If you’re covered through an employer, your HR or benefits team is your best friend. If you’re using the Marketplace, look for

local navigators or brokers who can help you compare plans. Many offer free assistance funded by federal or state programs.

3. Compare your options, not just your premiums

When you’re rushed, it’s tempting to grab the cheapest monthly premium and move on. But also check:

- Network: Are your doctors and preferred hospitals in-network?

- Prescription coverage: Are your regular medications covered at a decent tier?

- Deductibles and out-of-pocket maximums: How much could you pay in a bad year?

4. Keep copies of everything

Save PDFs, screenshots, emails, and confirmation numbers. If anything goes sidewayslike a missing application or a disputed datethose

records can save you hours of frustration.

5. Revisit other benefits at the same time

A qualifying life event is a good reminder to update:

- Life insurance beneficiaries.

- Retirement plan contributions.

- Emergency contacts and next-of-kin details.

If your life has changed enough to trigger a QLE, it might also be time to adjust your broader financial and protection plans.

Real-World Experiences with Qualifying Life Events

To make all this more concrete, let’s look at how qualifying life events play out in everyday lifeand what people often wish they’d

done differently.

“We got married…and then realized we only had 30 days”

Many couples are surprised to learn how short the QLE window can be with employer coverage. Picture this: you have a beautiful

wedding, go on your honeymoon, come home to a pile of laundryand somewhere under the travel receipts is a benefits packet you never opened.

By the time you dig it out, it’s day 28. You suddenly realize you have two days to decide which employer plan to keep, what

level of coverage you want, and which dependents go where. It’s stressful, but it’s also a great reminder:

- Ask both employers about their plan options and deadlines before the wedding.

- Compare total out-of-pocket costs, not just premiums.

- Decide who will carry coverage for the household so you’re not scrambling at the last minute.

“I turned 26 and learned the hard way about timing”

Aging off a parent’s plan at 26 is a classic qualifying life event. Many people assume their coverage will last through the end of their

birthday month or even the yearbut that’s not always true. Plans vary; some end coverage at the end of the month, others exactly on

the birthday.

The smart move is to:

- Check the exact end date on your current coverage several months before your birthday.

- Start shopping for Marketplace or employer coverage early so your new plan starts as soon as the old one ends.

- Look into income-based subsidies or Medicaid if your income is lower, especially early in your career.

“We moved to a new state and our old plan vanished”

Health insurance networks are often state-based. One family moved from one state to another for work, expecting to keep their

familiar insureronly to learn that the plan simply didn’t exist in their new ZIP code. Suddenly, their pediatrician and specialists

were out-of-network.

Because their move counted as a qualifying life event, they got a Special Enrollment Period to choose a new plan in their new state.

But they wished they had:

- Checked which insurers and networks were strong in the new area.

- Asked their current doctors if they were in-network for any plans in the new state.

- Budgeted for the possibility of higher premiums or different deductibles after the move.

“I lost my job, but assumed I was stuck until open enrollment”

Another common scenario: someone loses a job and the employer plan along with it. They know COBRA is an option, but the premium

feels outrageousafter all, they’re now paying the full cost of the employer plan plus an administrative fee.

What they may not realize is that this loss of coverage is a qualifying life event that opens up:

- Marketplace plans with potential premium tax credits.

- Medicaid or CHIP, depending on income and family size.

- Short-term coverage in some states, as a limited-purpose stopgap (with important limitations).

The key lesson: losing job-based coverage doesn’t automatically mean COBRA is your only path. Comparing your options during the

Special Enrollment Period can save you serious money.

Emotional side: benefits decisions in the middle of chaos

It’s easy to discuss qualifying life events like a neat checklist, but in real life, they’re often messy and emotional. Birth, death,

divorce, job loss, and big moves are some of the most stressful things people go through. Nobody wakes up after a sleepless night

with a newborn thinking, “Can’t wait to log into the benefits portal.”

That’s why it helps to:

- Lean on professionalsHR, navigators, brokers, or trusted financial advisors.

- Ask questions even if you think they’re “dumb.” The rules are complicated; it’s literally someone’s job to walk you through them.

- Break the task into small steps: confirm the date, gather documents, compare a couple of core plans, submit the application.

A qualifying life event is a reminder that your benefits should move with your life, not the other way around. With a bit of planning,

good information, and a calendar reminder or two, you can use these rules to protect yourself and your family instead of being surprised by them.

Bottom Line

A qualifying life event is any major changelike losing coverage, getting married, having a child, moving, or changing eligibility

for other programsthat unlocks a Special Enrollment Period outside regular open enrollment. Understanding what counts, how long

you have to act, and what documentation you need can help you make smarter, calmer decisions when life is anything but calm.

You can’t control when life throws big changes your way. But you can control how quickly you respond, how carefully you compare your

options, and how well your coverage matches your new reality.