Table of Contents >> Show >> Hide

- What Made the 1987 Crash So Special?

- So Would a Repeat Be That Bad Today?

- Why a Modern Replay Might Be Less Catastrophic Than 1987

- The Bigger Risk: A 1987-Style Drop with a 2026 Twist

- What Investors Usually Get Wrong About Crash Risk

- Final Verdict: Bad, Yes. 1987-All-Over-Again, Probably Not.

- Extended Perspective: What an 1987-Style Crash Would Feel Like in Real Life

- Conclusion

Wall Street loves a dramatic callback, and few market moments are more dramatic than Black Monday in 1987. One trading day. One historic plunge. Enough panic to make even seasoned investors consider learning a simpler hobby, like beekeeping. So the question is fair: if the market suffered another one-day collapse on that scale, would it really be that bad?

The honest answer is yes, but probably not in the exact same way people imagine. A repeat of the 1987 stock market crash would be painful, chaotic, and deeply unsettling. It would rattle retirement accounts, punish leveraged bets, freeze nerves, and send financial TV into full fireworks mode. But today’s market is not the market of 1987. The plumbing is different. The safeguards are stronger. The information moves faster. Ironically, that last part is both comforting and terrifying.

To understand whether a modern Black Monday would be catastrophic or merely brutal, you have to look at what actually happened in 1987, what changed afterward, and what new risks have quietly replaced the old ones.

What Made the 1987 Crash So Special?

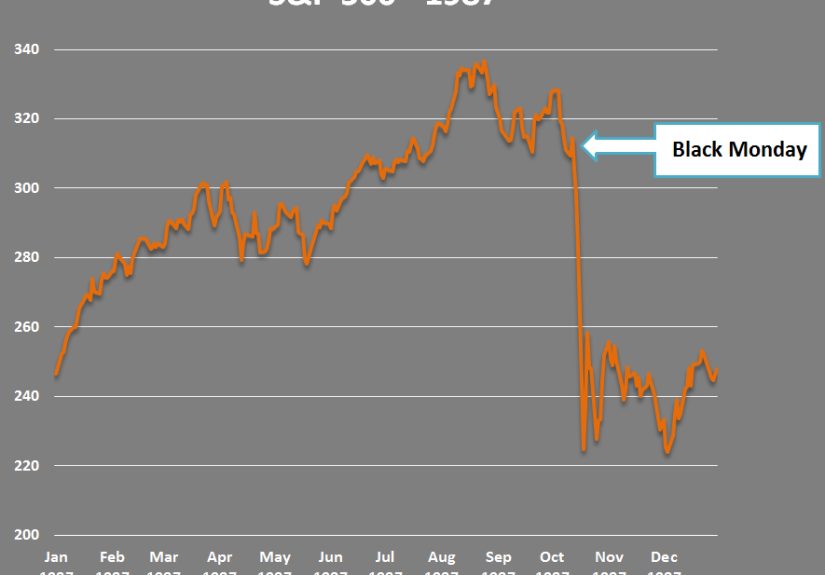

The crash of October 19, 1987, still holds a strange place in financial history. It was huge, sudden, and global. The Dow Jones Industrial Average fell 22.6% in a single session, a percentage drop so large that modern investors tend to read it twice just to make sure a decimal point was not misplaced.

What makes Black Monday so fascinating is that it was not a perfect replay of 1929, and it was not a banking collapse like 2008. It was a market structure event wrapped inside a confidence crisis. Stocks had already run up sharply before the crash, valuations looked stretched, interest-rate worries were building, and concerns about trade deficits and the dollar were adding tension. Then selling accelerated through portfolio insurance strategies and program trading, which were supposed to reduce risk but instead acted like a stress multiplier once everyone headed for the exits at the same time.

When “Risk Management” Helped Make Things Worse

One of the enduring lessons of 1987 is that tools designed to manage risk can become risk when too many people use them the same way. Portfolio insurance was marketed as a disciplined strategy. In practice, it often meant selling into weakness through stock-index futures as prices fell. That can work in a calm market. In a stampede, it can feel like trying to put out a grease fire with a leaf blower.

The infrastructure of the era also struggled. Trading systems were slower, coordination across markets was weaker, and price discovery became messy as volume surged. In other words, 1987 was not just a story about fear. It was a story about a market that was not fully prepared to process fear at scale.

So Would a Repeat Be That Bad Today?

Yes. A one-day drop anywhere near 1987 levels would still be ugly. Investors would lose trillions in paper wealth, margin calls would hit fast, and consumer confidence would take a punch. Even if the broader economy held up better than headlines suggested, the short-term pain would be very real.

That said, “bad” is not the same as “system-ending.” A modern crash would likely be less about the market mechanically breaking in the way it did in 1987 and more about how the shock spread through portfolios, sentiment, credit, and algorithms. The damage would depend on what caused the plunge in the first place. A technical unwind is one thing. A crash caused by recession fears, policy error, war, or a credit seizure is a much nastier animal.

Why It Would Hurt More Than People Think

First, household exposure to markets is broad. Many Americans do not day-trade from a neon-lit command center, but they do own stocks through 401(k)s, IRAs, target-date funds, pensions, and index funds. A severe one-day collapse would hit not only speculators but teachers, engineers, small-business owners, and anyone planning to retire on something sturdier than crossed fingers.

Second, modern markets are psychologically fragile in a new way. In 1987, investors waited for news. Today, they are submerged in it. Phones buzz. Apps refresh. Social media manufactures confidence and panic at industrial speed. A sharp selloff no longer arrives once on the evening news. It arrives every four seconds, in high definition, with opinion threads attached. That can intensify emotional selling even if the underlying financial system remains intact.

Third, market concentration matters. A handful of mega-cap stocks now carry enormous weight in broad indexes. That means weakness in a small cluster of giant names can drag passive portfolios, retirement funds, ETFs, and sentiment all at once. A crash that starts in crowded leaders can spread faster than many investors expect, not because every company is broken, but because so many portfolios are built on the same foundation.

Why a Modern Replay Might Be Less Catastrophic Than 1987

Here is the hopeful part: the market learned from Black Monday. Not perfectly, because Wall Street never misses a chance to invent a fresh kind of headache, but meaningfully.

Circuit Breakers Exist for a Reason

After 1987, regulators and exchanges built mechanisms designed to slow panic. Today’s market-wide circuit breakers pause trading when the S&P 500 falls by certain thresholds. These halts are not magical shields. They do not erase losses or restore optimism. What they do is create time. And in a panic, time is underrated. Time lets firms check exposures, investors breathe, market makers recalibrate, and humans briefly catch up with machines.

There are also single-stock volatility controls, such as the limit up-limit down framework, which aim to prevent individual securities from trading in absurd air pockets. These are the financial equivalent of guardrails on a mountain road. Guardrails do not stop bad driving, but they can reduce the odds that one bad turn becomes a multi-car disaster.

The Fed and Market Authorities Now Have a Playbook

In 1987, authorities had to improvise under pressure. Today, central banks, exchanges, regulators, clearinghouses, and major financial institutions have decades of crisis memory. They have studied 1987, 2008, the 2010 flash crash, the COVID panic of 2020, and every other episode that made traders age in dog years.

That matters. A crash can still be severe, but the official response is likely to be faster, more coordinated, and more publicly visible. Liquidity support, communication, margin oversight, and cross-market coordination are now much more central to the crisis toolkit than they were in the late 1980s.

Markets Have Already Been Stress-Tested Since Then

One useful reality check is this: modern markets have already faced serious stress events. The COVID selloff in 2020 triggered market-wide halts. The system looked shaky at moments, but it did not simply snap in half. Trading resumed. Prices found levels. Policymakers intervened. Investors, after a period of panic and handwringing, did what investors often do: they adjusted, complained, and went right back to refreshing charts.

That does not prove the next crash will be easy. It does suggest that the post-1987 safeguards are not theoretical decorations. They have been used in real conditions.

The Bigger Risk: A 1987-Style Drop with a 2026 Twist

The more interesting question is not whether the next crash would look exactly like 1987. It probably would not. The real question is what a modern market crash would attach itself to.

If the selloff were mostly technical, driven by positioning, leverage, or crowding, it could be violent but recoverable. If it exposed something deeper, such as a credit problem, a recession already underway, or a serious policy mistake, then the market drop would be a symptom rather than the disease. In that case, the one-day crash would be bad not because it resembled 1987, but because it announced that something underneath the market was already cracking.

There is also a structural irony in today’s market. Technology has made markets more transparent and more accessible. It has also made them more synchronized. Passive investing, ETF trading, algorithmic strategies, and real-time sentiment loops can improve efficiency in normal times while increasing crowding in stressed ones. That does not mean passive investing is dangerous by default. It means diversification can look beautifully boring right up until the day boring turns out to be genius.

What Investors Usually Get Wrong About Crash Risk

Many investors assume the worst damage comes from the drop itself. Often, the bigger damage comes from the reaction to the drop. Selling after a violent decline, abandoning a long-term plan, doubling down with leverage, or confusing a liquidity event with the end of capitalism are all classic ways to turn temporary pain into permanent regret.

That does not mean investors should shrug at crash risk. It means they should prepare for it when markets are calm, not invent a plan while the screen is glowing red like a toaster oven. Sensible position sizing, adequate cash reserves, diversified exposure, and realistic expectations are still boring, still unfashionable, and still wildly effective.

Final Verdict: Bad, Yes. 1987-All-Over-Again, Probably Not.

So, would a repeat of the 1987 crash really be that bad? Absolutely. A one-day plunge of that magnitude would be financially painful, emotionally exhausting, and politically noisy. It would hit portfolios fast and confidence even faster.

But it would not necessarily mean the financial system was doomed or that the economy was headed for a 1930s sequel. The biggest lesson from Black Monday is not that markets are fragile beyond repair. It is that fragility changes shape. In 1987, the danger came from crude market plumbing, coordinated selling strategies, and overwhelmed infrastructure. Today, the danger is more likely to come from concentration, speed, leverage, and the way modern investors all seem to receive the same memo at once.

In other words, a modern replay would still be bad. It would just be bad in updated software.

Extended Perspective: What an 1987-Style Crash Would Feel Like in Real Life

A modern crash would not be experienced as a single elegant number on a chart. It would feel personal almost immediately. A young investor checking a retirement app before work might see a balance fall by an amount that took a year to save. A near-retiree would not be thinking about market history or valuation bands; they would be doing frantic math at the kitchen table, wondering whether retirement now means sixty-five or seventy.

Financial advisers would spend the day acting like part strategist, part therapist, and part emergency dispatcher. Their phones would light up with variations of the same question: “Should I sell everything?” Traders would watch spreads widen and liquidity thin out in the most crowded names. CFOs at public companies would suddenly care a lot more about financing conditions. Politicians would discover a fresh desire to sound reassuring while sounding vaguely alarmed. Television anchors would speak in that solemn tone normally reserved for hurricanes and constitutional crises.

For ordinary workers, the strange thing about a crash is how abstract and immediate it can be at the same time. You can still go to lunch. Traffic still exists. The coffee shop still charges too much for oat milk. And yet, in the background, something important has shifted. Confidence is leaking out of the system. People delay big purchases. Executives pause hiring plans. Investors who felt rich on Friday suddenly feel cautious on Monday afternoon.

Then there is the digital layer. In 1987, panic spread through phones, terminals, and news reports. Today it would spread through push notifications, livestreams, group chats, meme accounts, brokerage apps, and hot takes from people whose credentials begin and end with “thread.” That means the emotional velocity of a crash could be faster than the financial velocity. Before the market even closes, millions of people would already have consumed several hours’ worth of fear.

Still, experience also suggests something else. Markets are dramatic, but investors are adaptable. After the initial shock, people start sorting themselves into camps. Some panic. Some freeze. Some buy. Some announce they were “waiting for this opportunity,” which is usually true in the same way everyone claims they were about to start stretching before the injury. Over time, the noise fades, portfolios get rebalanced, and the market starts doing what it has always done: repricing the future before most people are emotionally ready for it.

That is why the lived experience of a crash is so important. It is not just a test of market structure. It is a test of temperament. A repeat of 1987 would hurt, but it would also reveal who had a real plan and who merely had optimism wearing business casual. And that may be the most uncomfortable lesson of all.

Conclusion

The idea of another Black Monday makes for gripping headlines because it combines history, fear, and a giant red number. But the more useful question is not whether history can rhyme. It is whether investors, regulators, and institutions have learned enough to keep a rhyme from becoming a remake. The answer appears to be yes, at least partly. A repeat of the 1987 crash would still be severe, but the damage would likely be shaped less by broken market plumbing and more by modern crowding, speed, and psychology. For investors, that means the smartest response is not panic or denial. It is preparation.