Table of Contents >> Show >> Hide

- What Is Compound Interest?

- Simple Interest vs. Compound Interest: The Big Difference

- Why People Underestimate the Power of Compound Interest

- The Rule of 72: A Simple Way to Understand Growth

- Compound Interest Works Best With Three Ingredients

- A Practical Example: Small Monthly Savings, Big Long-Term Difference

- Compound Interest Can Also Work Against You

- Why Fees, Taxes, and Inflation Matter

- Compound Interest and Retirement Planning

- How to Use Compound Interest in Everyday Life

- The Psychology of Underestimating Compound Interest

- Common Mistakes That Reduce the Benefits of Compound Interest

- Experiences Related to Underestimating the Power of Compound Interest

- Conclusion: Do Not Let Small Beginnings Fool You

- SEO Tags

Compound interest is one of those financial ideas that sounds sleepy until it quietly walks into the room wearing a superhero cape. At first, it looks like nothing special: a little interest here, a few dollars there, maybe enough to buy a sandwich if the sandwich is feeling humble. But give compound interest enough time, and suddenly the small amounts you ignored start behaving like they took a motivational seminar.

The main reason people underestimate the power of compound interest is simple: the early results look boring. Human brains love quick wins. We notice a flash sale, a raise, a tax refund, or the dopamine sparkle of “free shipping.” But compound interest works slowly at first. It rewards patience, consistency, and the rare ability to not panic every time your financial plan looks like it is growing at the speed of a houseplant.

Yet this quiet force is one of the most important concepts in personal finance, long-term investing, savings growth, retirement planning, and wealth building. Whether you are saving for college, building an emergency fund, investing through a retirement account, or simply trying to make better money decisions, understanding compound interest can change how you see time, spending, and opportunity.

What Is Compound Interest?

Compound interest means earning interest not only on your original money, called the principal, but also on the interest that money has already earned. In plain English: your money starts making money, and then that money starts making more money. It is the financial version of a snowball rolling downhill, except less cold and usually better for your future.

For example, imagine you put $1,000 into an account earning 5% interest per year, compounded annually. After one year, you would have $1,050. The next year, you do not earn 5% only on the original $1,000. You earn 5% on $1,050. That gives you $1,102.50 after two years. The extra $2.50 may not sound dramatic, but that is exactly why compound interest is so easy to underestimate. The magic is not in one year. The magic is in year 10, year 20, year 30, and beyond.

Simple Interest vs. Compound Interest: The Big Difference

Simple interest is interest calculated only on the original principal. If you invest $1,000 at 5% simple interest, you earn $50 every year. After 10 years, you would have $1,500. Nice, tidy, predictableand about as exciting as a calculator with beige buttons.

Compound interest, however, keeps adding earned interest back into the balance. With the same $1,000 at 5% compounded annually, after 10 years you would have about $1,629. That extra $129 is the result of interest earning interest. Stretch the time to 30 years, and the difference becomes much bigger. Simple interest would bring the total to $2,500. Compound interest would grow it to about $4,322.

This is why the phrase “interest on interest” matters. The longer your money compounds, the more the growth comes from previous growth rather than from the original amount alone.

Why People Underestimate the Power of Compound Interest

1. The Early Years Look Too Small to Matter

The first stage of compound growth can feel painfully slow. If you save $100 and earn $5, nobody throws a parade. Your bank does not send balloons. Your future self does not appear in a glowing mist and say, “Excellent choice.” But that small beginning is where the entire process starts.

Many people quit too early because they expect financial growth to look dramatic right away. They compare slow compounding to fast spending. Spending gives instant proof: you bought the thing, you used the thing, the thing now lives in your closet judging you. Saving and investing, by contrast, require faith in a process you may not see clearly for years.

2. We Think in Straight Lines, But Compounding Is Curved

Most people naturally think in linear terms. If $100 grows by $5 in one year, we assume it will keep growing in neat little $5 steps. Compound interest does not move like that. It grows on a curve. At first, the curve is flat enough to look unimpressive. Later, it bends upward faster.

This is why long-term investing often feels boring at the beginning and powerful later. The mistake is assuming the early pace is the permanent pace. It is not. The early phase is the foundation. The later phase is where compounding starts flexing.

3. Waiting Feels Harmless

One of the most expensive phrases in personal finance is “I’ll start later.” It sounds reasonable. After all, later is not never, right? The problem is that compound interest treats time as fuel. When you delay, you do not just lose the money you failed to save. You also lose the years that money could have spent growing.

Consider two people. Person A invests $200 per month from age 25 to age 35, then stops adding money but leaves the account invested. Person B waits until age 35 and then invests $200 per month until age 65. Depending on the annual rate of return, Person A may still end up surprisingly close to, or even ahead of, Person B despite contributing far less total money. That is the power of starting early.

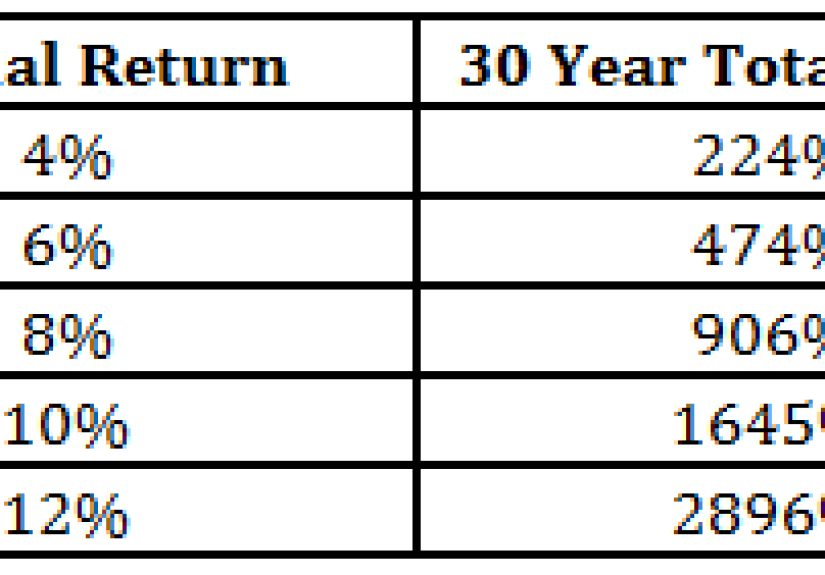

The Rule of 72: A Simple Way to Understand Growth

The Rule of 72 is a quick mental shortcut for estimating how long it takes money to double. You divide 72 by the annual rate of return. If your money earns 6% per year, it may take about 12 years to double. If it earns 8%, it may take about 9 years. If it earns 12%, it may take about 6 years.

This rule is not perfect, but it is useful because it makes compounding easier to picture. A $10,000 investment that doubles every 9 years could become about $20,000, then $40,000, then $80,000 over long periods, assuming the return is achieved and the money remains invested. The point is not to promise a specific result. The point is to show why time and rate of return are such important ingredients.

Compound Interest Works Best With Three Ingredients

Time

Time is the superstar. The earlier you begin saving or investing, the longer compound interest can work. Even small amounts can become meaningful when they have decades to grow. This is why financial educators often encourage young people to start early, even if they can only save a modest amount.

Consistency

Compound interest loves regular contributions. Saving $25, $50, or $200 every month may not feel exciting, but consistency builds momentum. Automatic transfers can help because they remove the need to make the same good decision repeatedly. Think of it as putting your future on autopilot, preferably not the kind of autopilot that flies into a snack aisle.

Rate of Return

The interest rate or investment return matters. A higher return can dramatically change long-term results. However, higher potential returns usually come with higher risk, especially in investments such as stocks or mutual funds. Savings accounts and certificates of deposit may offer stability, while stock market investments may offer higher long-term potential with more ups and downs. The right choice depends on your goals, timeline, risk tolerance, and financial situation.

A Practical Example: Small Monthly Savings, Big Long-Term Difference

Let’s say someone invests $150 per month for 30 years and earns an average annual return of 7%, compounded monthly. Over that time, they contribute $54,000 of their own money. But with compound growth, the account could grow to roughly $183,000 before taxes and fees. In this example, most of the final balance comes not from the original contributions but from investment growth.

Now imagine that same person waits 10 years and invests $150 per month for only 20 years. They would contribute $36,000, and at the same assumed return, the account could grow to about $78,000. The difference is not just the missing $18,000 in contributions. It is the missing decade of compounding.

This is the part that surprises people. Time does not simply add value. It multiplies opportunity.

Compound Interest Can Also Work Against You

Here is where compound interest removes the cape and puts on a tiny villain mustache. The same force that helps savings and investments grow can make debt grow too. Credit card balances, unpaid interest, and certain loans can compound against you if you carry balances for long periods.

When you owe money at a high interest rate, interest can be added to your balance, and future interest may be calculated on that larger amount. This is why minimum payments can feel like trying to empty a swimming pool with a teaspoon. You are doing something, technically, but the pool is not impressed.

Understanding compound interest is therefore not only about investing. It is also about avoiding expensive debt, comparing annual percentage yields, reading account terms, and noticing how fees or interest charges affect your long-term financial health.

Why Fees, Taxes, and Inflation Matter

Compound growth is powerful, but it does not operate in a fantasy land where fees do not exist and inflation politely stays home. Investment fees can reduce returns. Taxes can affect how much money you keep. Inflation can reduce purchasing power over time. A balance may look larger in dollars while buying less than expected if inflation has been high.

This is why it is important to pay attention to net returns, not just advertised rates. A fund with high fees may need stronger performance just to match a lower-cost option. A savings account with a low annual percentage yield may be safe but may not keep up with inflation. A tax-advantaged retirement account may help money compound more efficiently, depending on the account type and rules.

Compound Interest and Retirement Planning

Retirement planning is one of the clearest examples of compound interest in action. Many workplace retirement plans, individual retirement accounts, and long-term investment accounts rely on the idea that regular contributions plus time can create meaningful growth.

Employer matching contributions can make the effect even stronger. If an employer offers to match part of your retirement contribution, that match is essentially extra money added to your account. Once invested, it can also compound over time. Skipping a match can mean leaving future growth on the table, which is like refusing free pizza because you do not feel like opening the box.

The biggest retirement mistake many people make is assuming they can catch up easily later. Sometimes they can, but it usually requires much larger contributions. Starting earlier allows smaller contributions to carry more weight because time does part of the heavy lifting.

How to Use Compound Interest in Everyday Life

Start With a Clear Goal

Compound interest becomes easier to respect when it is connected to something real. Saving for a home, college, retirement, emergency expenses, a business, or financial independence gives the numbers emotional meaning. A goal turns compound interest from a math concept into a personal strategy.

Automate Your Savings

Automation is one of the most practical ways to benefit from compounding. Set up recurring transfers to a savings account, retirement plan, or investment account. When the process is automatic, you are less likely to forget, delay, or spend the money on something with a charging cable and questionable warranty.

Increase Contributions Over Time

You do not have to start with a huge amount. Begin with what you can manage, then increase contributions when your income rises or expenses fall. Even small increases can have a large impact when they are maintained for years.

Reinvest Earnings

Reinvesting dividends, interest, or other earnings allows those earnings to generate more growth. This is one of the core behaviors that makes compounding powerful. Taking earnings out too early can slow the process.

Be Patient During Market Volatility

Investments can rise and fall. Long-term investors often need patience, diversification, and a plan that matches their risk tolerance. Compound interest is not a guarantee of smooth growth. It works best when combined with disciplined behavior and realistic expectations.

The Psychology of Underestimating Compound Interest

People often underestimate compound interest because it asks us to value the future. That is harder than it sounds. A dollar today feels real. A larger amount years from now feels abstract. This is called present bias: the tendency to favor immediate rewards over future benefits.

Another challenge is that compounding is invisible day to day. You may not notice the effect after a week or a month. But wealth building often depends on repeated ordinary decisions: saving regularly, avoiding high-interest debt, keeping fees low, reinvesting earnings, and giving money time to grow.

The funny thing is that compound interest does not require genius. It requires behavior. You do not need to predict every market move or become the person at dinner who says “asset allocation” before the appetizers arrive. You need a reasonable plan, consistent contributions, and enough patience to let the math do its job.

Common Mistakes That Reduce the Benefits of Compound Interest

Starting Too Late

Waiting is the classic mistake. Many people postpone saving because the amount they can start with feels too small. But small amounts are exactly where compounding begins. The best starting amount is often not the perfect amount. It is the amount you can begin with now.

Stopping Too Soon

Compound interest rewards staying power. Constantly withdrawing money, pausing contributions, or switching strategies without a reason can interrupt growth. There are times when using savings is necessary, especially for emergencies, but long-term accounts work best when they remain long term.

Ignoring High-Interest Debt

Investing while carrying high-interest debt can be like filling a bucket while someone drills holes in the bottom. Paying down costly debt may provide a strong financial benefit because it stops interest from compounding against you.

Chasing Unrealistic Returns

Because compound interest is powerful, some people become tempted by promises of unusually high returns. Be careful. Real investing involves risk, and no legitimate investment can guarantee sky-high returns without trade-offs. If an opportunity sounds too perfect, it may be wearing tap shoes and waving a red flag.

Experiences Related to Underestimating the Power of Compound Interest

One of the most common experiences people have with compound interest is regret. Not dramatic movie-scene regret with rain on a window, but the quiet kind that shows up when someone finally runs the numbers. They realize that the $50 per month they thought was “too small to matter” could have become thousands of dollars over time. The lesson is not to feel guilty. The lesson is to begin where you are.

Many people first understand compound interest through a savings account. At first, the interest looks tiny. A few cents appear, then a few dollars. It is easy to laugh and say, “Well, I’m not retiring on that.” True, you are probably not buying a beach house with three months of savings interest. But the point is habit formation. When you regularly save and watch money grow, even slowly, you start building financial confidence. That confidence often leads to better decisions: comparing rates, avoiding unnecessary fees, and thinking more carefully before spending.

Another experience comes from investing. Someone may start a retirement account with a small paycheck contribution and feel underwhelmed. The balance moves up, then down, then sideways like it is trying to learn line dancing. For several years, it may not look impressive. Then, after steady contributions and reinvested earnings, the account begins to grow faster. The person realizes that the early years were not wasted. They were the quiet years when the foundation was being built.

Parents and teachers often see the “aha” moment when young people compare two savers: one who starts early and one who starts later. The early saver may contribute less total money but still ends up with a larger balance because compounding had more time to work. This example is powerful because it shows that money is not the only resource. Time is also a resource, and once it passes, it cannot be deposited retroactively. Sadly, banks do not offer a “missed decade” button.

There is also the less cheerful experience of debt. Many adults underestimate how fast interest can grow on credit cards or unpaid balances. A purchase that seemed manageable becomes expensive when interest is added month after month. This experience teaches the reverse lesson: compounding is neutral. It helps the owner of the interest. If you are earning it, wonderful. If you are paying it, the party is happening at your expense.

Some people discover the power of compound interest when they increase contributions gradually. They may begin with $25 per month, then raise it to $50, then $100 after a raise. The change feels painless because it happens slowly. Years later, they see that these small increases made a major difference. This is one of the most encouraging parts of personal finance: improvement does not always require a heroic sacrifice. Sometimes it requires a calendar reminder, automatic transfer, and the wisdom to leave the money alone.

The deepest experience is emotional. Compound interest teaches patience in a world that sells urgency. It reminds us that slow progress is still progress. It rewards the person who keeps going when the results are not yet impressive. In that sense, compound interest is more than a formula. It is a financial habit, a mindset, and a quiet vote for your future self.

Conclusion: Do Not Let Small Beginnings Fool You

Underestimating the power of compound interest is easy because the beginning looks so ordinary. A few dollars of interest. A small monthly contribution. A retirement account that does not seem exciting yet. But over time, those ordinary decisions can become extraordinary results.

The key is to start early, stay consistent, reinvest earnings, manage risk, avoid high-interest debt, and respect the role of time. Compound interest is not magic, but it can feel magical when you finally see the long-term results. It is math with patience baked in.

So the next time someone says, “It’s only a small amount,” remember that small amounts are where big financial stories often begin. Compound interest does not shout. It whispers for years, then eventually clears its throat and says, “Surprise.”

Note: This article is for educational and informational purposes only. It synthesizes widely accepted financial education concepts from reputable U.S. consumer finance, investor education, banking, and economic education resources. It is not personal financial, tax, or investment advice.